Investors who are familiar with Baker Steel’s investment views will know that we, along with many others, believe there can be “no net zero without mining”. No sector exemplifies this sentiment as well as the copper industry, as momentum builds for the green energy transition. Copper is the indispensable commodity required for electrification, from electric vehicles (EVs) to renewable energy production, transmission and storage.

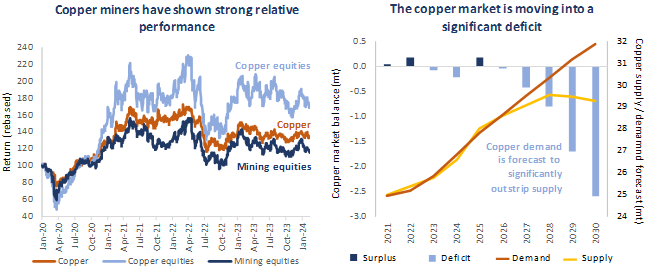

Only a few months ago, the copper market was not expected to go into deficit until towards the end of the decade, however recent supply issues due to production disruption and guidance downgrades now indicate a deficit for 2024. This deficit is expected to grow to 2.6mt by 2030, representing 9% of total supply. In our view, a squeeze on the copper market is now a real possibility in the near-term.

Copper mining equities are among the purest ways for investors to gain exposure to the green energy transition, and they currently appear undervalued having seen their share prices come under pressure in recent months due to the mixed outlook for global growth. Yet the copper sector is well-supported for growth, regardless of short-term economic forecasts. Having exceeded expectations in recent years, the roll-out of electric vehicles and expansion of green energy capacity continues to gain momentum. With supply challenges set to continue, higher incentive prices will likely be needed to encourage production of this critical green metal.

Do higher copper prices and a re-rating of copper equities lie ahead?

Rising demand – Copper demand is forecast to rise 23% by 2030, driven by the energy transition alongside broader industrial usage. In particular, ex-China copper demand is forecast to accelerate.

Supply constraints – Production disruption, guidance downgrades, permitting issues and falling grades have become key supply issues. Current copper pricing does not incentivise new production.

Imminent deficit – The copper market is in deficit in 2024, with this shortfall projected to deepen in the years ahead. Without higher prices, the copper market is forecast to reach a 9% supply deficit by 2030.

The opportunity in copper equities – Copper miners represent a pure way to play the green energy transition and we see substantial upside potential in this sub-sector. However, given the technical, CAPEX and political risks around copper mining, an active management approach is required.

Figure 1

Source: RBC, Wood MacKenzie, Baker Steel internal research

Few metals could boast such significance for the global economy as copper. As a key industrial metal, the copper market often provides a diagnosis of the health of the global economic outlook. Yet it is the metal’s role in electrification which places it uniquely at the centre of the green energy transition. Alongside a range of other speciality metals, copper faces steep demand forecasts in the near-future alongside transformational long-term demand trends. The market’s current mixed consensus on copper, based on a weak economic growth outlook, may be about to shift sharply amid growing supply constraints. As the copper market enters a deficit in 2024, we believe the near-term opportunity is skewed significantly in favour of a copper “squeeze” and outperformance by copper miners.

Historic demand for critical metals – How much copper is needed for the green energy transition?

Copper is utilised across almost all areas of green technology. A single 1mw solar panel requires 4.5t of copper, alongside 35-45t of steel and 3.5-8t aluminium. A wind turbine (1mw) requires 2-12t of copper, with amounts varying based on factors such as on-shore vs. offshore, alongside 85-210t of steel, 1-2t of aluminium and c.200kg of rare earths. Meanwhile an EV requires up to 80kg of copper, around 3.5x the amount used in an internal combustion engine vehicle, along with 900kg of steel, 280kg of aluminium and c.40kg of battery metals (notably lithium and cobalt)[i].

Figure 2

Sources: IEA, World Energy Outlook 2023 & 2019. Note, forecast EV sales based on stated policies and electric car targets of the world’s 20 largest car manufacturers. Electric vehicles comprise of battery electric vehicles (BEV) and plugin hybrid vehicles.

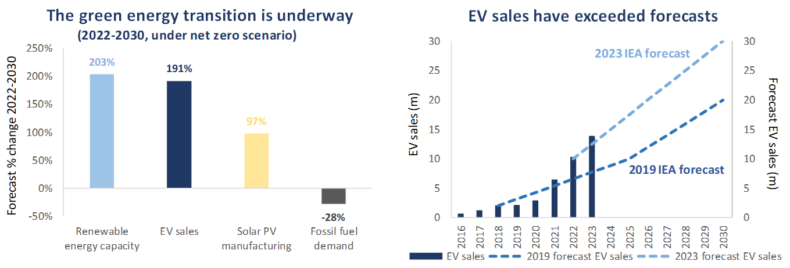

The investment case for copper and copper miners is underpinned by the growth of green technology and its forecast expansion in the years ahead. The green revolution has gained significant momentum in recent years. Renewable energy capacity is forecast to increase by over 200% by 2030, while solar photovoltaic manufacturing is forecast to rise 97% by the end of the decade. With regard to the growing EV market, sales are forecast to increase by almost 200% by 2030. Since launching our Electrum strategy in 2019, the pace of the green transition has surpassed our expectations. As illustrated above, EV sales forecasts from the IEA based on stated policies have been upgraded significantly, with annual sales now forecast to reach 30m by 2030, 10m vehicles higher than 2019 forecasts[ii].

While factors relating to the broader global economic outlook remain influential for the direction of copper prices, we consider that the pace of change in green technology is an increasingly significant driver. Rio Tinto forecasts annual total demand growth for copper of 3.9% (CAGR) between 2022 and 2035, with a broadly equal net demand uplift from traditional demand and energy transition demand.

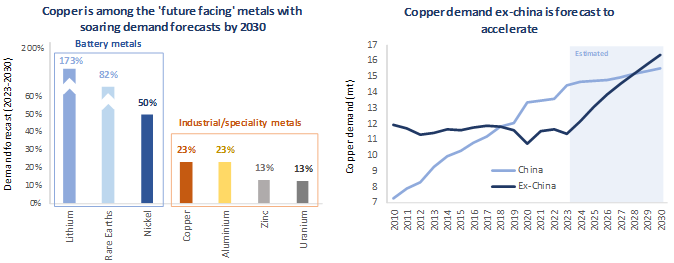

Overall, copper demand is forecast to rise 23% by 2030, placing it among the “future facing” metals which face significant demand growth driven by the green energy transition[iii]. Producers of these metals and materials are the focus of Baker Steel’s Electrum strategy, offering investors exposure to the historic growth potential of these sectors. China’s outlook is of particular significance given the country currently consumes 57% of global copper supply alongside producing 45% of supply[iv]. Yet projections for the coming years indicate that ex-China demand will outpace Chinese demand, and later this decade is even forecast to surpass Chinese demand.

Figure 3

Sources: Industry reports, BMO Capital Markets, Canaccord Genuity, CRU, BNEF

Supply constraints are growing – Is a copper shortage looming?

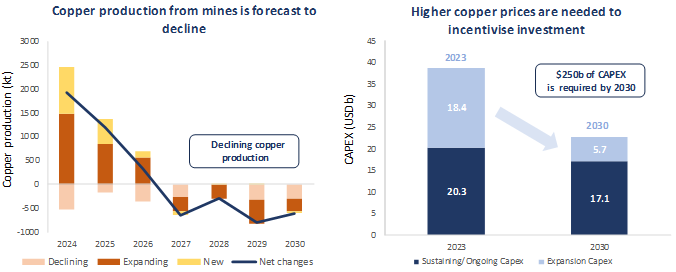

Against the backdrop of rising demand for copper, the sector faces a tight supply outlook. As with most speciality and industrial metals, copper has a rapidly shifting supply and demand dynamic as nascent green industries experience strong growth amid a varied supply response. Until recently, forecasts indicated a surplus in the copper market in 2024 due to the number of projects coming online, with deficits only expected towards the end of the decade. However, the outlook for copper supply has now shifted, with current forecasts indicating a mild deficit for 2024, growing towards a substantial deficit of 2.6mt by 2030, representing c.9% of global copper supply[v]. This shift in expectations for coppers’ deficit increases the likelihood that copper prices will rise sooner than anticipated, to incentivise new production.

The causes of copper’s imminent supply shortage are primarily production disruption and guidance downgrades by major producers, yet longer term the trends towards falling grades, shorter mine life and longer permitting timescales all present challenges to new copper supply. In addition, volatile copper prices pose a further headwind for producers. Overall, these challenges result in a lack of incentives for miners to develop new copper projects, while a substantial number of large copper projects which were due to be delivered are now delayed.

Recent production disruption has had a material impact on the outlook for copper supply. A significant recent development for the sector was Panama’s requirement that First Quantum Minerals, a major producer, suspend production at its Cobre Panama copper mine, leaving substantial uncertainty over the timeline for its potential reopening. Cobre Panama was expected to produce 385kt of copper in 2024, representing 1.75% of global copper supply[vi]. A further major development for copper supply has been Anglo American’s cut in production guidance for 2024, due to geotechnical issues. The company reduced guidance by around 195kt, equating to almost 1% of global supply. In addition, BHP’s delayed production growth at its Escondida copper mine due to permits and studies provides another example of the copper market’s supply challenges. The impact of disrupted copper supply can be seen in treatment and refining charges, which have fallen by more than half over the past six months. This decline tells us there is a shortage of raw copperconcentrate coming from mines and demand for concentrate is now growing faster than mine supply.

Alongside recent supply disruption, the longer-term trends of falling grades, shortening mine life and longer development times continue to cause existing copper assets to disappoint. Copper grades have fallen c.24% over the past 20 years, with current grades averaging just 0.5%[vii]. The lack of new meaningful copper deposit discoveries has been accompanied by more challenging geology, increased ESG scrutiny, and rigorous environmental permitting, increasing the timescale and cost of delivering new supply. Today the average lead time from discovery to commercial production is almost 16 years, with permitting alone potentially taking nearly a decade[viii].

Figure 4

Sources: Wood Mackenzie, RBC. Data as at Q4 2023 Scenario. Production note, "Declining", "Expanding" and "New" based on 2023 classification. CAPEX note, includes all copper mine costs, revenue and residual cash-flow (US$): Base Case plus Probable projects.

Average copper mine life has also declined significantly, having fallen -27% over the past decade from 37 years to around 27 years. Looking ahead at the potential for new copper supply, we see that production growth will slow in the years ahead before entering a decline from 2027 onwards. As illustrated on the chart above, even mines which are currently classed as “new” or “expanding” move into decline within the next four years.

The result of these supply issues is that investment in new copper production is insufficient to reach production goals. While ongoing CAPEX is forecast to decline slightly by 2030, expansion CAPEX is expected to fall almost 70% by 2030, to just USD 5.7b[ix]. The supply challenges facing the copper sector represent a significant problem for the green energy transition. As new grades fall, development costs rise and permitting timelines extend, higher incentive prices are needed for copper miners, to encourage new production.

What does the copper squeeze mean for miners?

The case for investment in the copper sector not only remains firmly intact but has been strengthened in the near-term by supply-side challenges. The copper squeeze which was largely expected later this decade has been accelerated, strengthening the outlook for copper miners during a turbulent time for mining equities. Meanwhile the medium- to longer-term secular trends of electrification and the green energy transition remain core drivers for the copper sector.

As active investment managers we identify a number of copper producers which offer value as well as growth, with good project pipelines. A potential recovery of investor interest in copper miners would come against a backdrop of depressed sentiment towards the sector. Copper equities would have to rise by around 70% just to regain all-time highs[x], yet in our view this recovery would only be the start of the historic re-rating we believe lies ahead for copper miners alongside broader speciality and industrial metals mining equities. If the world is to decarbonise, estimates indicate that 6.5b tonnes of metals will be needed between now and 2050[xi]. Miners’ investment levels are currently too low to ensure this and the current supply issues facing the copper industry highlight many of the broader challenges across the mining sector.

A positive development for the copper sector has been increased media and investor interest in the metal’s link to the green revolution, helping to raise its profile. Recent copper discoveries by a company backed by Jeff Bezos and Bill Gates highlights the potential for the copper sector given its significance to technological development. Meanwhile recently announced investments in the mining sector by Elliott Investment Management, which is reportedly committing USD 1b to mining assets, and Stanley Druckenmiller, who has dumped tech stocks in favour of mining equities, in this case gold stocks, demonstrates that the mining sector can capture the attention of high-profile investors.

As is the case across commodity markets, supply and demand dynamics for copper will fluctuate in the years ahead. Yet we see both near-term catalysts as well as long-term supportive trends for copper, backed by what we believe is the start of a new commodity supercycle driven by the green energy transition. Baker Steel’s Electrum strategy, which invests in the producers of metals and minerals for a sustainable future, is currently overweight copper equities given the positive outlook we see for this sub-sector. As we approach what we believe will be a supportive environment for much of the mining industry in the months and years ahead, Baker Steel’s team continues to deliver our unique and value driven investment approach, to the benefit of our clients, while adhering to sector leading ESG practices.

[i] Rio Tinto. Onshore versus Offshore wind. Framed versus frameless panels. EV requirements assume an average battery size of 55kWh (2021).

[ii] IEA, World Energy Outlook 2023

[iii] BMO Capital Markets

[iv] Nornickel, 2023 estimates

[v] RBC, WoodMacKenzie

[vi] First Quantum Minerals, Company Reports

[vii] Wood Mackenzie, data 2001-2021

[viii] The Economist

[ix] Wood Mackenzie

[x] Based on the performance of the Global X Copper Miners ETF

[xi] Energy Transitions Committee

About Baker Steel Capital Managers LLP

About Baker Steel Capital Managers LLP

Baker Steel Capital Managers LLP manages three award winning investment strategies, covering precious metals equities, speciality metals equities and diversified mining.

Baker Steel has a strong track record of outperformance relative to its peers and relative to passive investments in the metals and mining sector. BAKERSTEEL Precious Metals Fund is the 2025 winner of the GELD-Magazin Alternative Investment Award, and 2025 winner for the seventh year running of the Lipper Fund Awards while BAKERSTEEL Electrum Fund is the 2025 winner of the Euro Fund Awards Commodity Equities Performance over 10 years. The Baker Steel Resources Trust has also been named Investment Company of the Year 2021, 2020, 2019, Natural Resources, by Investment Week.

Fund Managers Mark Burridge and David Baker have been awarded two Sauren Gold Medals for 2021 and were awarded Fund Manager of the Year at the 2019 Mines & Money Awards.

Important

Please Note: This document is a financial promotion is issued by Baker Steel Capital Managers LLP (a limited liability partnership registered in England, No. OC301191 and authorised and regulated by the Financial Conduct Authority) for the information of a limited number of institutional investors (as defined in the Fund prospectus) on a confidential basis solely for the use of the person to whom it has been addressed. This document does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe or purchase any shares or any other interests nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefor. Recipients of this document who intend to apply for shares or interests in Baker Steel’s funds are reminded that any such application may be made solely on the basis of the information and opinions contained in the relevant prospectus or other offering document relating thereto, which may be different from the information and opinions contained in this document. This report may not be reproduced or provided to any other person and any other person should not rely upon the contents. The distribution of this information does not constitute or form part of any offer to participate in any investment. This report does not purport to give investment advice in any way. Past performance should not be relied upon as an indication of future performance. Future performance may be materially worse than past performance and may cause substantial or total loss.