The brave new world of industrial growth – A golden age for miners?

Looking through the fog of uncertainty, pro-growth policies focused on infrastructure, enabling technologies and the energy transition are poised to drive a demand boom for critical raw materials.

Governments worldwide are grappling with geopolitics, conflict and economic headwinds, from high debt and sluggish productivity to strained public finances. The common solution amongst policymakers is to push to reignite economic growth. From policies to encourage inward investment in the US and state intervention in China, to vast infrastructure projects across the Middle East and defence spending in Europe, policymakers are working to stimulate and shield their domestic industries. This global growth push is fuelling the “new industrial revolution”, a wave of rapid technological change powered by AI, robotics, and clean energy. The result is a potent mix of industrial policy and metals-intensive innovation, all set against a backdrop of sticky inflation and fragile raw material supply chains.

Global shocks, from war in Ukraine and the Middle East to the fallout from Trump’s tariffs, have underscored the strategic importance of critical materials and gold, along with the vulnerabilities of global supply chains. In this landscape, precious metals have already entered a new upcycle, buoyed by robust physical demand from a range of investors from central banks to family offices and private individuals. Other sub-sectors, such as copper and uranium show signs of tight supply-demand balances, whilst others such as rare earths are receiving a geopolitical boost. For investors, mining equities’ undervaluation coupled with powerful demand trends creates some compelling opportunities in a sector critical to the next era of global growth.

Amid a global push for growth, key themes for metals and mining include:

- Policy – Governments are rolling out ambitious, but varied, growth strategies with a focus on infrastructure, fiscal policy, tariffs, energy security, domestic industries and defence.

- Technology – Clean energy, AI, digital infrastructure, robotics, aerospace and defence are all driving demand for critical metals.

- Supply – Metals’ supply is constrained by geology, permitting, ESG and supply side discipline. Supply chains are being reconfigured by reshoring efforts, geopolitics, amid a regional concentration of output.

- Value – Many miners have strong balance sheets and are deeply undervalued, despite capital discipline.

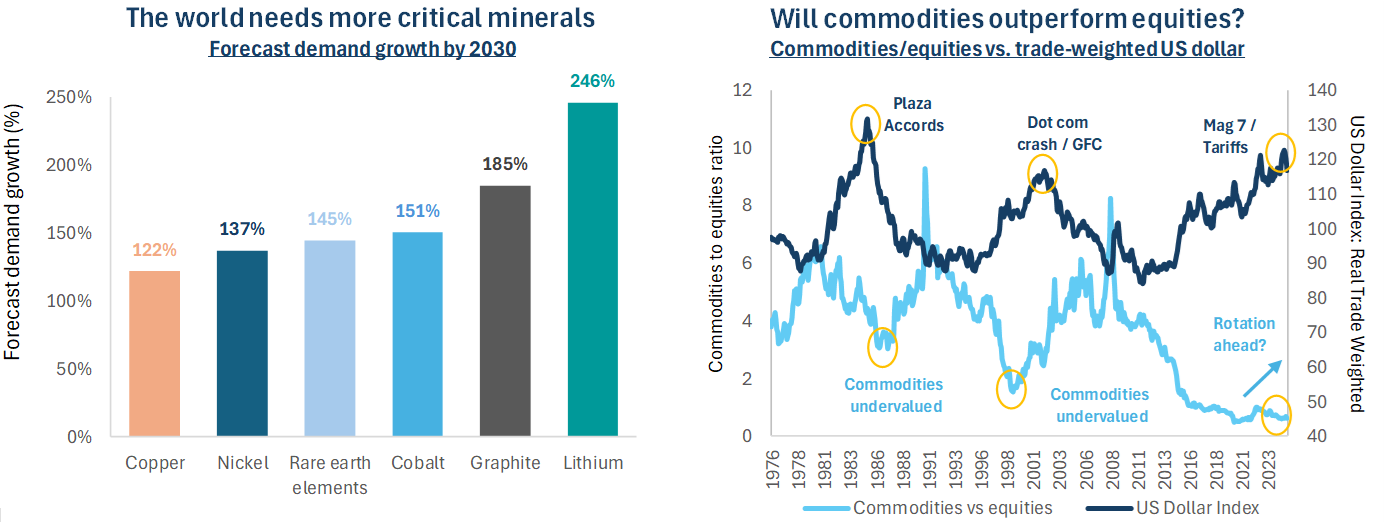

Figure 1

Source: Bloomberg, IEA. Note Forecast demand growth based on Announced pledges scenario. Data at 31 May 2025.

Global pro-growth policies signal a strong outlook for metals demand. While bulk commodities will benefit from renewed infrastructure spending, it’s the critical raw materials required for new technology, the digital economy and the energy transition which are set to see particularly sharp demand growth. As highlighted on the chart above, the International Energy Agency (“IEA”) forecasts lithium could surge 245% between 2024 and 2030 under its “Acknowledged Pledges” scenario, with copper, nickel, rare earths, cobalt, and graphite forecast to rise by 122–185% over the same period[i]. With such explosive growth forecasts, the mining sector faces a transformation in the years ahead. The push for industrial growth is happening at a time when commodities and mining equities have significantly de-rated versus broader equity markets, as shown on the chart above, highlighting a sector that remains undervalued, even as its strategic importance grows.

The prospect of a synchronized global push for growth carries significant implications for commodity markets. Today, the US, China, EU, and Gulf Cooperation Council (“GCC”) are all pursuing industrial growth, but via distinct approaches, reflecting their unique political systems, economic models, natural resources, and strategic goals. The common thread is a renewed focus on domestic production and energy security, creating a structurally supportive environment for the metals and mining sector.

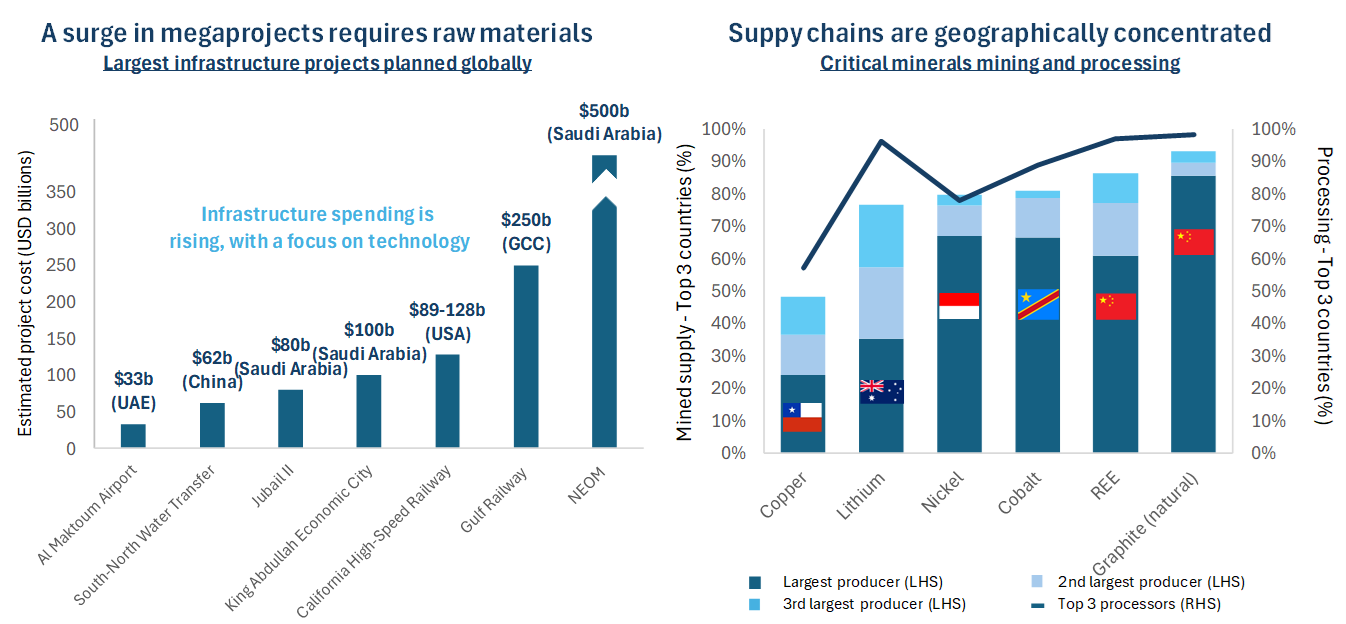

Figure 2

Sources: Baker Steel Capital Managers LLP, IEA, Blackridge Research and Consulting, Baker Steel Capital Managers LLP. Data at 31 May 2025.

United States: Market-Led Growth Meets Mounting Fiscal Strain

The US is pursuing a market-driven growth strategy, with government support through incentives, infrastructure investment, and fiscal policy. Following legislation such as the 2022 CHIPS and Science Act, hundreds of billions have been directed towards building supply chains for hi-tech manufacturing, critical raw materials and on reshoring. Deregulation, such as expedited permitting, and tariffs continue to support US-based critical mineral production, offering clear upside for domestic miners. Infrastructure investment has shifted under Trump 2.0, pivoting away from the green initiatives funded by Biden’s Inflation Reduction Act and instead focusing on increasing investment in traditional infrastructure. However, the financial risks are mounting for the US. Trump’s “Big, Beautiful Bill”, which covers a multitude of investments and tax cuts, is poised to add further strain, increasing deficits and debt loads. US net interest payments are forecast to reach 4.6% of GDP by 2025, well above the UK (1.6%) and Germany (0.6%)[ii]. Moody’s recent downgrade of US sovereign credit highlights this deteriorating financial backdrop. For gold investors this is compelling, with weaker fiscal fundamentals and potential easing by the US Fed supporting gold’s appeal as a safe-haven asset and inflation hedge. Broader commodities also face a positive outlook in an environment of dollar pressure and inflationary growth.

China: State-Led Growth with a Strategic Technology Focus

China remains committed to state-led industrial growth, with a focus on infrastructure, real estate, and high-tech manufacturing. Its dual circulation strategy focused on boosting domestic demand while preserving export competitiveness. The Belt and Road Initiative has extended China’s industrial footprint globally, while policies promote rapid growth in technology, most notably AI and robotics. In the wake of tariff disputes with the US, China retains powerful tools to reignite growth, most likely stimulus in the format of credit expansion via state banks. As the world’s largest consumer of commodities, China’s growth trajectory has direct implications for metals markets. Its dominance in future-facing technologies is striking, with over 70% of global EVs, 80% of solar panels, and 70% of lithium-ion batteries produced in China[iii]. This reinforces long-term demand for speciality metals tied to clean energy and automation.

GCC: Mega-Projects and Resource-Driven Transformation

The GCC countries are undertaking some of the world’s most ambitious infrastructure investments, aiming to diversify away from hydrocarbons. Saudi Arabia’s Vision 2030 is anchored by mega-projects such as NEOM, Qiddiya, and the Red Sea Project, designed to build the country’s technology, tourism, finance and renewable energy industries. While some project ambitions have recently been scaled back, even a moderated execution carries significant implications for metals demand. NEOM alone is reported to be consuming 20% of the world’s steel output, alongside massive demand for copper, aluminium, concrete, and glass[iv]. Plans to invest USD 100 billion by 2035 in domestic mining signal the country’s intent to become a key player in critical mineral supply chains[v]. The UAE is similarly focused on infrastructure development, including green technology, with Masdar City targeting 100% renewable energy[vi]. Furthermore, GCC Sovereign Wealth Funds are channelling petrodollars into domestic projects and global strategic assets.

European Union: Regulation-Led Growth with Green Ambitions

Europe faces structural challenges when it comes to growth, due to ageing demographics, low productivity, and underinvestment. The EU is focused on regulatory reform and targeted stimulus to promote growth, improve sustainability and support digital transformation. The European Green Deal aims to make the EU climate-neutral by 2050, backed by carbon pricing and renewable energy investment. Meanwhile, the EUR 750 billion NextGenerationEU fund (running through 2026) supports electric mobility, energy efficiency, and digital infrastructure[vii].

Figure 3

Source: IEA Global Critical Minerals Outlook 2025, Blackridge Research and Consulting (November 2024).

This synchronized push for growth, investment, and supply chain resilience is structurally bullish for commodities. The last time we saw a similar alignment was in the early 2000s, when China’s rapid industrial expansion coincided with robust US economic growth, triggering a powerful upcycle across commodity markets. More recently, the 2022 Inflation Reduction Act demonstrated the power of targeted industrial policy, delivering USD 370 billion in US subsidies for clean energy, electric vehicles (“EV”), and domestic manufacturing and driving a surge in battery metals’ prices[viii].

Amid strong demand trends for raw materials, supply side growth faces challenges, particularly for critical minerals which often face geographic concentration of mining and processing. As highlighted on the chart above, the top three mining jurisdictions for copper, lithium, nickel, cobalt, rare earths and graphite, account for between c.50-90% of mined supply. On the processing side, the picture is similar with the top three jurisdictions accounting for over 80% of battery metals processing[ix]. China has steadily ramped up export controls on a broad range of critical metals, often targeting the US through bans or tight licensing. China maintains quotas on rare earths exports, while graphite exports to the US also face tight scrutiny and strict end-use vetting[x]. Since December 2024, Chinese exports of gallium, germanium and antimony to the US have been banned, with stricter annual licensing regimes now enforced, while February 2025 saw additional critical metals, tungsten, tellurium, bismuth, indium, and molybdenum added to its list of exported minerals requiring licenses[xi].

The New Industrial Revolution is boosting metal intensity – Can miners meet soaring demand?

Rollout of many new technologies have consistently outpaced expectations. Solar energy is a prime example of how rapid technological change can impact the raw materials it consumes. Between 2024 and 2030, solar photovoltaic is expected to account for 80% of the growth in global renewable capacity and by the end of this decade solar is set to become the largest renewable source[xii]. The silver sector is poised to be a core beneficiary of this rapid growth. A solar panel contains around 20g of silver and, while substantial thrifting has reduced the silver weighting in most solar panels, new cell technologies are using larger amounts. TOPCon cells use c.30-75% more silver than a typical panel, while HJT cells potentially use more than twice a typical panel’s weighting[xiii].

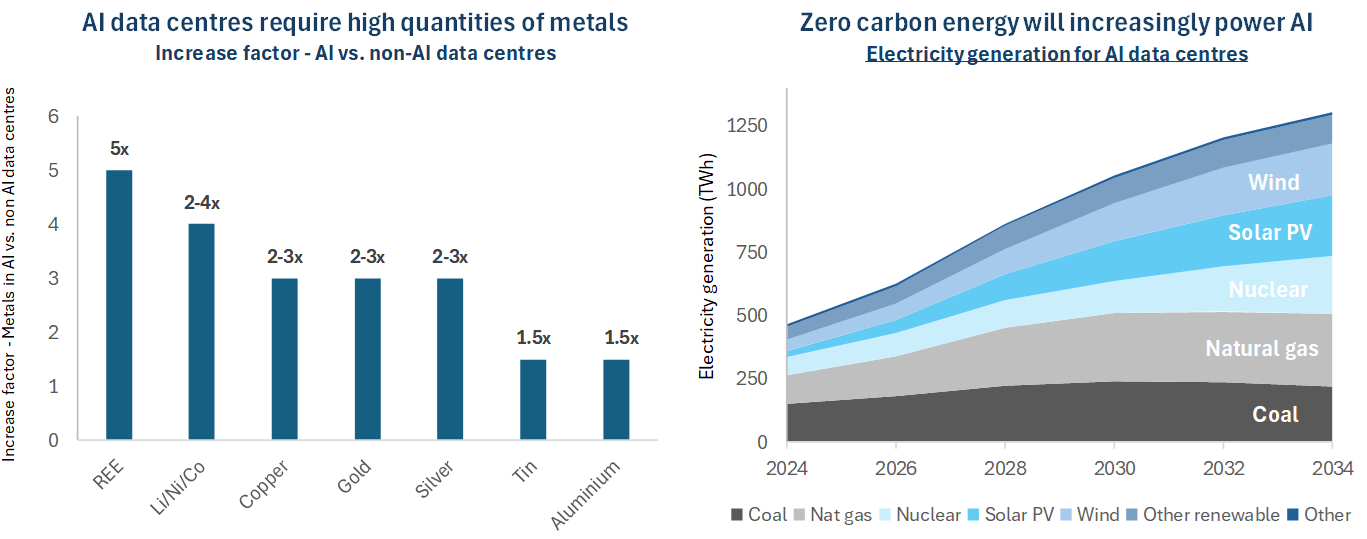

AI is another area of rapid technological growth, which holds substantial implications for metals demand. Global investment in data centres has nearly doubled since 2022 and amounted to half a trillion dollars in 2024[xiv]. A typical AI-focused data centre consumes as much electricity as 100,000 households, but the largest ones under construction today may consume 20 times as much[xv]. As shown on the chart below, AI data centres consume substantially more metals than conventional data centres. Five times as much rare earth elements (“REE”) are required, as well as two to four times as much lithium, nickel and cobalt. Copper, gold and silver are also used in AI data centres in quantities two to three times higher than in non-AI data centres.

Figure 4

Source: International Copper Association, IEA, BSRIA & ICA, McKinsey & Company, U.S. Department of Energy, Adamas Intelligence, Roskill, Uptime Institute, TechInsights, BloombergNEF, Schneider Electric, Vertiv.

Other green technologies, notably EVs, have seen more mixed recent growth results relative to many analysts’ lofty expectations for the sector. Global EV sales reached c.17 million in 2024, a 25% increase from 2023, continuing the global surge which has catapulted EVs into the mainstream over the past decade[xvi]. EVs now account for over 20% of all new passenger car sales globally in 2024. Demand for EVs continues to be driven by China which accounted for nearly two-thirds of global EV sales in 2024, in contrast to the European market which has seen EV sales growth slow due to the removal of subsidies[xvii]. Alongside rapid EV adoption, a similar growth pattern can be seen in battery demand, which has surged to over 1 TWh in 2024, having exhibited transformational growth over the past decade, boosted primarily by EV demand for batteries as well increasingly by stationary storage demand[xviii].

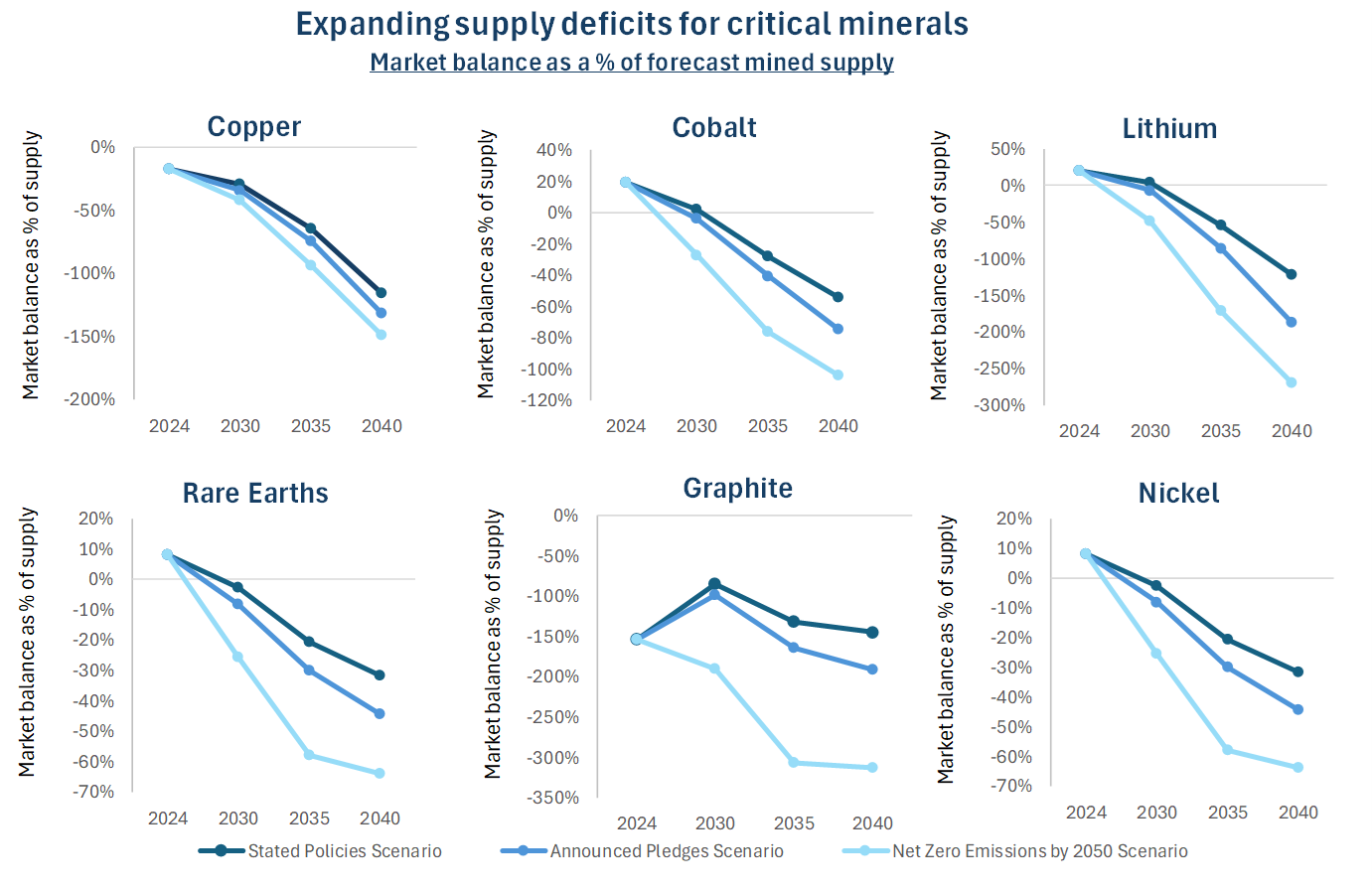

The secular demand growth trend remains intact for those metals required for the new industrial revolution. The supply side, however, faces questions over whether demand growth can be met in the years ahead. Miners face an array of challenges to boost production, from permitting timelines to increasingly stringent environmental rules in some jurisdictions. Overall, a lack of exploration spending for many metals has limited production outlook. The explosion of demand for battery metals, lithium, cobalt, nickel, have caused supply of these metals to expand rapidly, pushing the market balance into temporary surplus. Yet, as shown on the charts below, current surpluses for battery metals and a selection of other critical metals are forecast to descend into supply deficit in the coming years, as current supply projections fail to keep pace with demand forecasts. Under each of the IEA’s three scenarios, “Stated Policies”, “Announced Pledges” and “Net Zero Emissions 2025”, substantial deficits are forecast to open up in the 2030s, should further policies to reduce emissions be implemented.

Figure 5

Source: IEA, Baker Steel Capital Managers LLP. Note, graphite demand based on all grades, supply based on battery grade.

A profitable sector with a strong growth outlook – Why are miners undervalued?

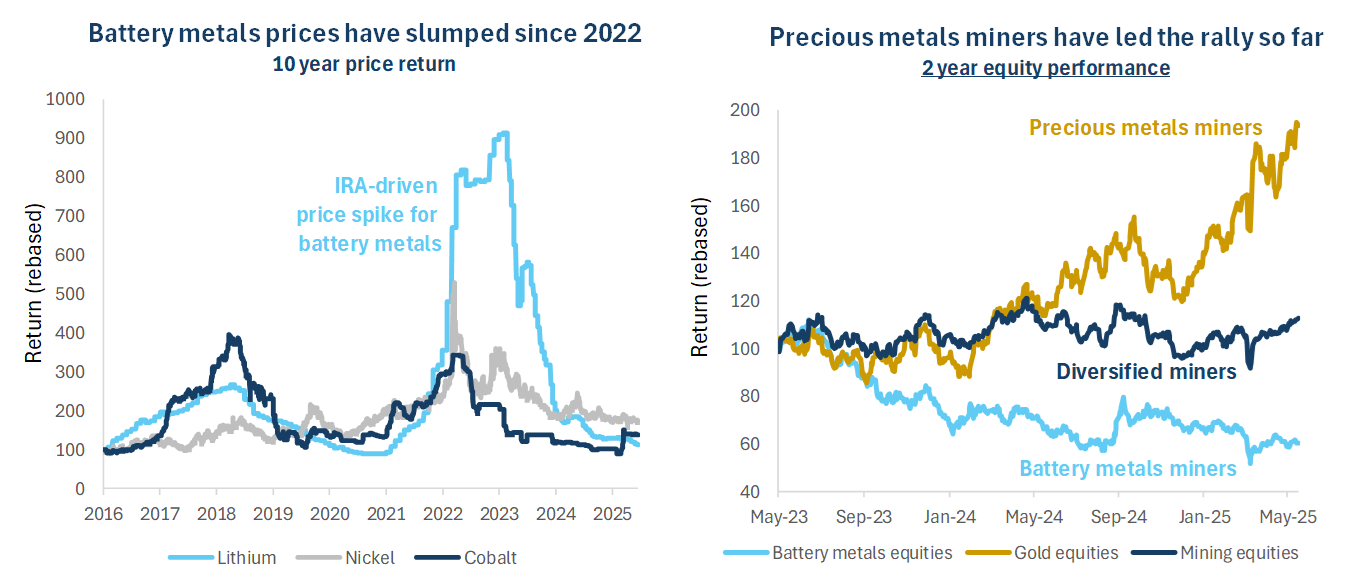

Despite supportive demand trends, mining equities have faced a broad de-rating compared to general equity markets in recent years. We believe this situation presents a significant value opportunity for investors seeking to capitalise on the long-term trends of pro-industrial growth policies, the new industrial revolution, and the clean energy transition. Despite producing the critical raw materials needed for new technology, battery metals miners have faced steep share price declines, primarily due to temporary oversupply following a ramp-up of production in recent years, and due to a tempering of investor sentiment towards green technologies.

Lithium prices have declined -87.7% since their 2023 highs, while nickel and cobalt prices have fallen -67.2% and -55.9% respectively since their highs in 2022[xix]. During this volatile period, the performance of mining equities has diverged strongly. Battery metals miners have seen their share prices almost half over the past two years, in contrast to precious metals miners which have almost doubled during this period, while diversified miners’ performance has essentially been flat[xx].

Figure 6

Source: Bloomberg. Data at 17 June 2025.

Mining equities appear undervalued compared to the broader equity market on several fronts. Looking at market multiples, miners currently trade at 6.0x EV/EBITDA, compared to 17.8x for technology stocks, 13.2x for industrials and 12.4x for healthcare[xxi]. Despite their recent run, precious metals miners are still trading at even lower valuations, at just 5.6x EV/EBITDA. Our view is that these low valuations are unjustified given the financial health of the mining sector. Operating margins are strong, and in the case of precious metals miners significantly higher than most equity sector, at 30.1%[xxii]. Free cash flow yields for the mining sector also currently exceed broader equity markets, with further growth forecast[xxiii].

Miners’ undervaluation comes down to a few factors. Uncertainty over global growth in recent years, as interest rates rose around the world, trade tension increased and the USD strengthened, has resulted in a lack of interest in the metals sector from western investors due to their focus on mainstream equities. Many investors, particularly in the west, have missed out on the initial phase of the new bull market for metals and mining, which has seen the precious metals sector lead the way so far. Investor concerns remain over the costs and capital discipline in the sector, however Q1’25 results have highlighted cost control, margin expansion and, in the case of precious metals miners, increasing buybacks. As metals prices continue to rise, or hold at high levels, we believe there will be a catch up as company results continue to indicate miners’ strong financial positions. Importantly, it only takes a small rotation from mainstream equities to generate big flows into the sector.

In our view the mining sector holds material upside potential in the months and years ahead, as pro-growth policies and the new industrial revolution drive demand for metals and as mining companies demonstrate strong profitability. However, it is essential to differentiate between companies based on fundamentals such as asset quality, operational events and risk factors, alongside top-down factors, such as commodity-specific trends and geopolitics. Active investment management, as undertaken by Baker Steel Capital Managers LLP, has a track record of generating enhanced returns in the metals and mining sector. Whilst volatility is likely to remain, we believe that Baker Steel’s strategies are well-positioned to thrive, as active management and nimble asset allocation allow our funds to navigate risk and rewards during times of volatility, uncertainty and opportunity.

Sources:

[i] IEA, Global Critical Minerals Outlook 2025.

[ii] OECD, Bloomberg.

[iii] IEA, Global Critical Minerals Outlook 2025.

[iv] Arabian Gulf Business Insight.

[v] BMO Global Metals, Mining, and Critical Minerals Conference, Eng. Khalid Al-Mudaifer, Deputy Minister of Industry and Mineral Resources for Mining Affairs.

[vi] Masdar.

[vii] European Commission.

[viii] Bloomberg, Baker Steel Capital Managers LLP.

[ix] IEA, Global Critical Minerals Outlook 2025.

[x] CSIS, S&P.

[xi] S&P.

[xii] IEA, Energy and AI, April 2025.

[xiii] Apmex, Sprott.

[xiv] IEA, Energy and AI, April 2025.

[xv IEA, Energy and AI, April 2025.

[xvi] IEA, Global EV Outlook 2025.

[xvii] IEA, S&P.

[xviii] IEA, McKinsey.

[xix] Bloomberg, data in USD terms as at 17 June 2025.

[xx] Bloomberg, data in USD terms as at 17 June 2025.

[xxi] Bloomberg, data as at 30 May 2025. Based on MSCI Equity sectors.

[xxii] Bloomberg, data as at 30 May 2025. Based on MSCI Equity sectors.

[xxiii] Bloomberg, data as at 30 May 2025.

About Baker Steel Capital Managers LLP

About Baker Steel Capital Managers LLP

Baker Steel Capital Managers LLP manages three award winning investment strategies, covering precious metals equities, speciality metals equities and diversified mining.

Baker Steel has a strong track record of outperformance relative to its peers and relative to passive investments in the metals and mining sector. BAKERSTEEL Precious Metals Fund is the 2025 winner of the GELD-Magazin Alternative Investment Award, and 2025 winner for the seventh year running of the Lipper Fund Awards while BAKERSTEEL Electrum Fund is the 2025 winner of the Euro Fund Awards Commodity Equities Performance over 10 years. The Baker Steel Resources Trust has also been named Investment Company of the Year 2021, 2020, 2019, Natural Resources, by Investment Week.

Fund Managers Mark Burridge and David Baker have been awarded two Sauren Gold Medals for 2021 and were awarded Fund Manager of the Year at the 2019 Mines & Money Awards.

Important

Please Note: This document is a financial promotion is issued by Baker Steel Capital Managers LLP (a limited liability partnership registered in England, No. OC301191 and authorised and regulated by the Financial Conduct Authority) for the information of a limited number of institutional investors (as defined in the Fund prospectus) on a confidential basis solely for the use of the person to whom it has been addressed. This document does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe or purchase any shares or any other interests nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefor. Recipients of this document who intend to apply for shares or interests in Baker Steel’s funds are reminded that any such application may be made solely on the basis of the information and opinions contained in the relevant prospectus or other offering document relating thereto, which may be different from the information and opinions contained in this document. This report may not be reproduced or provided to any other person and any other person should not rely upon the contents. The distribution of this information does not constitute or form part of any offer to participate in any investment. This report does not purport to give investment advice in any way. Past performance should not be relied upon as an indication of future performance. Future performance may be materially worse than past performance and may cause substantial or total loss.