Strategic competition for critical metals – What does it mean for miners?

From rare earths to uranium and battery metals, strategic investment in critical metals and minerals supply chains is increasing, creating opportunities for miners.

Competition for supplies of critical metals is a defining feature of today’s industrial and political landscape, amid rising demand from technologies from electrification to AI and clean energy. In this report we address the strategic and supply chain issues for rare earth elements (“REEs”), the policy support and rising demand for uranium, and consider whether the lithium sector is near a turning point. Geopolitical tensions, re-shoring, and export controls have highlighted the vulnerability of critical metals supply chains. Recent US government deals with several producers of these critical metals have put the mining sector in the spotlight.

Growth from metals-intensive technologies associated with the “New Industrial Revolution” present opportunities for active investors in the mining sector. As a commodity-equity specialist, Baker Steel’s strategies have benefitted from meaningful exposure to producers of critical metals, such as copper, uranium and silver, which were all added to the US critical minerals list this month[i], alongside REEs. We believe active stock selection, nimble asset allocation, and robust risk management make our strategies advantageous for investors seeking exposure to this fast-growing and sometimes volatile sector.

Critical metals face secular demand trends and vulnerable supply chains –

- Demand from technology – From AI to EVs and clean energy, technologies associated with the “New Industrial Revolution” have a high intensity of use of critical metals.

- Concentrated supply – Western governments are striving to reshore supply chains, currently dominated by China. Recent US government deals with producers highlight the strategic significance of critical minerals.

- Opportunity and risk – REE and uranium have been significant contributors to Baker Steel’s Electrum strategy during 2025, alongside silver and copper, as part of an actively managed value-driven

Rare earth elements – Strategic interests meet supply chain risks

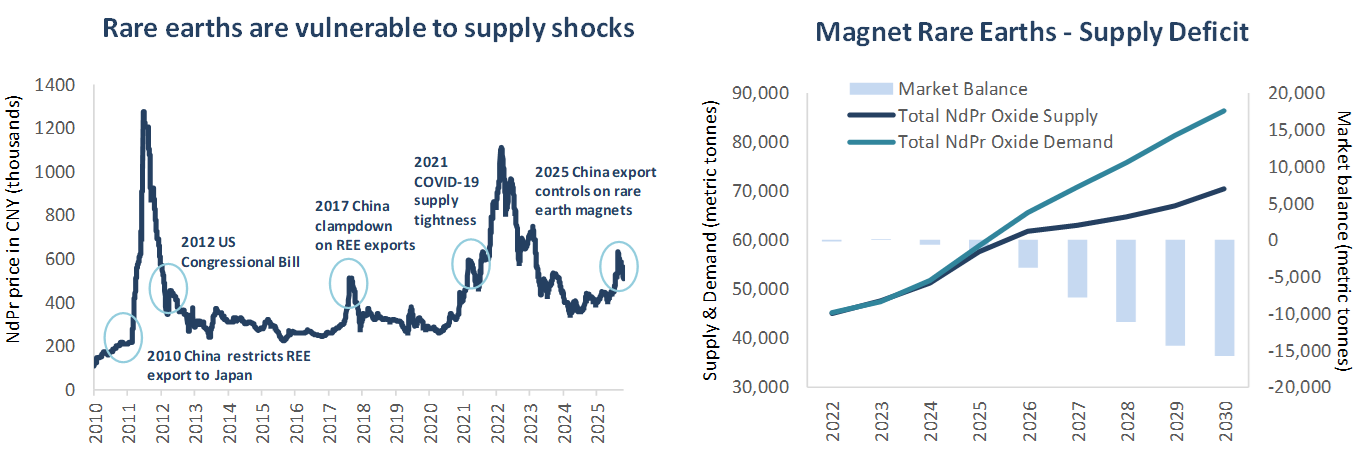

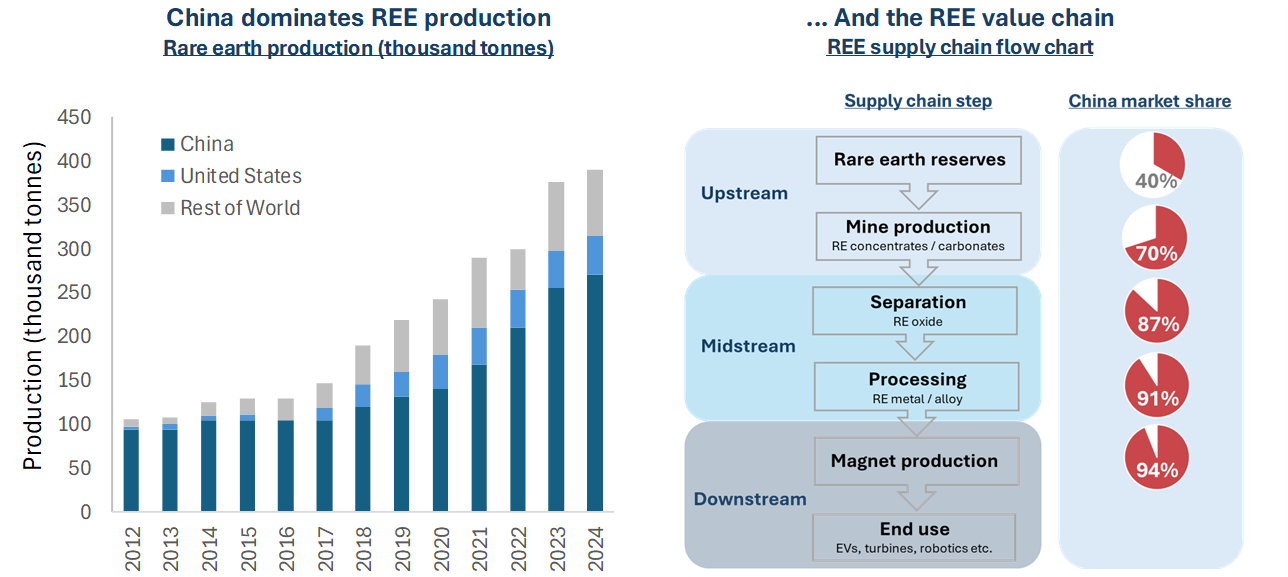

No group of commodities better represent the strategic challenges and opportunities in critical metals than REEs, which sit at the crossroads of electrification, defence, and high-performance electronics. Of these 17 elements, the magnet metals are particularly sought after. As a group, REEs share similar geochemical properties and occur together geologically. They are mined and undergo several processing steps together before being separated into individual oxides through multiple additional chemical processes. The sector faces a supply deficit in the years ahead, while prices have historically been prone to spike on supply side risks and geopolitical factors.

Figure 1

Source: Bloomberg, Canaccord Genuity.

As shown in the chart above, neodymium (Nd) and praseodymium (Pr), the two primary light REEs used in permanent magnets, are already in supply deficit, a shortfall expected to widen to c.22% of total supply by 2030 as demand rises 46%[ii]. The key heavy REEs, dysprosium (Dy) and terbium (Tb), which enhance high-temperature magnet performance, are also forecast to remain in a structurally tight market.

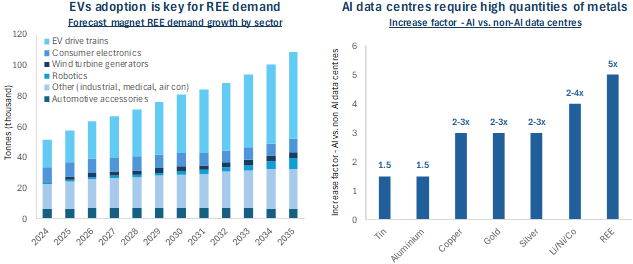

EVs are currently the largest source of demand for magnet REEs, accounting for roughly one-third of demand today and projected to rise to c.57.8% by 2035[iii]. Most EVs use NdFeB permanent magnets, a blend of NdPr, iron (Fe), and boron (B), which offer strength and are lighter than other magnets. Around 80% of EV motors rely on these REE magnets, typically containing 1-2 kg of material. While EV motors can be built without REEs, the alternatives are generally less efficient and reduce driving range[iv]. A second major growth driver is wind power, where high-efficiency permanent magnets are essential for turbines. A single wind turbine can require 250 kg or more of neodymium (BMO). With global wind capacity expected to roughly double by 2030[v], this sector represents a robust, secular tailwind for REE demand, alongside rising requirements for other critical metals.

Aside from magnets, industrial demand for REEs covers a wide range of uses, from screens and LED lighting in consumer electronics, to battery technology, and usage in the chemicals industry and in glass making. A notable area of growth for REE, and other critical metals is in AI data centres, which require a high intensity of metals use. An AI data centre can use 5x as much REEs as a non-AI data centre, alongside 2-4x the quantities of battery metals and 2-3x as much copper, gold and silver[vi].

Figure 2

Source: Bloomberg NEF, Canaccord Genuity estimates, IEA, AI Insight Media, Trafigura, Reuters, Microsoft, BMO, Ivanhoe Mines.

Beyond industrial uses, government demand for REE magnets is also substantial. The US Department of Defense is expected to increase its demand for NdFeB magnets from c.200tpa today to between 500tpa and 1.5ktpa by 2030[vii]. The strategic importance of REEs and the vulnerabilities within their supply chains has been brought into sharp focus by President Trump during both of his terms, alongside broader concerns over critical minerals security. While China’s dominance across critical mineral supply chains is well known, REEs represent an especially acute challenge due to their strategic significance in defence, energy, and advanced technologies.

Rising geopolitical tension, concerns over intellectual property, and the high concentration of supply are prompting governments to take an increasingly active role in the REE sector. A pivotal moment came in July 2025, when the US Department of Defense announced a USD 550 million landmark partnership with MP Materials, the United States’ sole domestic REE producer and a holding within Baker Steel’s Electrum strategy[viii]. The agreement funds expansion of heavy REE separation capacity at MP’s Mountain Pass mine in California, as well as additional magnet manufacturing capacity. The deal is particularly significant because the USD 110/kg price floor is significantly above current spot prices, signalling a challenge to China’s influence over global pricing through its upstream control. While not a full bifurcation of markets, the US government’s commitment to a price floor and supporting investment is a move away from persistently range-bound, low REE prices. This represents a meaningful tailwind for Western producers, supporting investment, new supply, and greater resilience in the value chain.

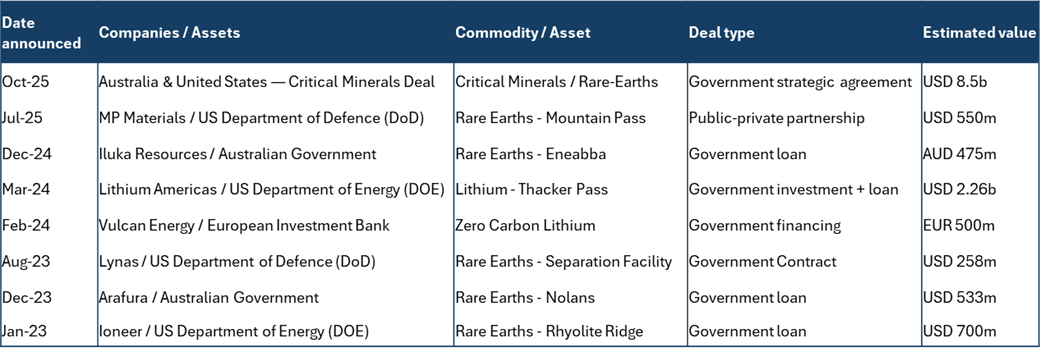

As shown in the table below, the US government has executed a series of critical minerals agreements alongside the MP Materials partnership, including a REE contract with Australia’s Lynas Rare Earths. These initiatives mark significant steps as the US increases its involvement in a strategically sensitive sector.

Critical Minerals – Examples of Recent Government Deals

Figure 3

Source: Company reports, FT, ABC News, Reuters.

Alongside direct government initiatives, US policy has also helped catalyse commercial deals aimed at rebuilding REE capacity onshore. In recent months, Pensana announced an offtake agreement with eVAC, which operates a magnet-making facility in South Carolina[ix]. Meanwhile, magnet manufacturer Vulcan Elements has struck agreements with both Energy Fuels, to secure US sourced rare earth oxides exclusively, and ReElement Technologies, a domestic REE processor, to scale up the US magnet supply chain[x].

The US has entered national level agreements with Australia and Malaysia, key sources of ex-China REE supply. The critical minerals deal between the US and Australia, announced in October 2025, establishes a framework for deeper integration between Australian producers and US supply chains. Similarly, a recent US-Malaysia deal established cooperation on critical minerals, including REEs, with Malaysia agreeing not to ban or impose quotas on exports of processed REEs to the US[xi]. Beyond the US, the EU is also providing support for critical minerals supply chains. September saw the inauguration of NEO Performance Materials’ magnet factory in Estonia, which received support from the EU. This factory will be Europe’s largest producer of rare-earth permanent magnets, potentially satisfying 15% of the EU’s magnet demand[xii]. Meanwhile Japan, the largest ex-China REE magnet manufacturer, continues to support its domestic industry through financing and offtake agreements, as is deepening frameworks with the US[xiii].

Despite Western efforts, China’s dominance of the REE supply chain is unlikely to be displaced in the near term. Although REEs are relatively common in the Earth’s crust, with the term “rare” reflecting their typically low concentrations rather than scarcity, they are difficult to extract and complex to separate. Establishing new separation facilities, processing plants, and magnet manufacturing capacity will take many years, even with government support. As illustrated in the graphic below, the REE value chain is overwhelmingly concentrated in China, which accounts for c.70% of global mined supply, c.91% of processing capacity, and c.94% of permanent-magnet production[xiv].

Figure 4

Source: USGS, Minerals Yearbook 2016-20 & Mineral Commodity Summaries 2023-25, BMO Capital Markets, Baker Steel Capital Managers LLP, Center for European Policy Studies, Industry Reports.

This entrenched position underscores the scale of the challenge facing Western supply-chain rebuilding efforts. While the US leads in intellectual property for many advanced technologies, China retains control over the manufacturing technology and exercises influence across the REE value chain through production quotas and tax policy. Even as China’s headline economic growth moderates, policymakers remain focused on high-tech industrial expansion aimed at achieving technological self-sufficiency and global leadership in innovation and advanced manufacturing. Strategic priorities such as AI, semiconductors, aerospace, and renewable energy imply a high intensity of metals use ahead.

As both the largest producer and consumer of REEs, China is expected to continue prioritising its domestic needs, utilising export controls and other protectionist tools, particularly as companies like Huawei compete for supplies. From smartphones and EV manufacturing to its maglev transit systems, China’s economic and technological ambitions rely heavily on REEs and other critical minerals.

Recent de-escalation between the US and China, following Chinese REE export restrictions imposed in response to U.S. tariffs, demonstrates that compromise can be reached, even if temporarily. However, history shows that supply chains are vulnerable to geopolitical tension, as illustrated by China’s two-month suspension of REE exports to Japan in 2010 after a territorial dispute in the East China Sea[xv]. Whether President Trump’s negotiation style ultimately eases or heightens these tensions remains to be seen. What is clear is that if the US is to pursue a genuine industrial and manufacturing renaissance, it will require secure supply chains for REEs and other critical metals.

As an active manager, Baker Steel has traded around the listed REE miners as the policy environment has evolved. The policy-driven buildout of non-China REE supply, from mining to separation and magnet manufacturing, is investable and likely to endure across multiple political cycles, given its alignment with defence, industrial strategy, and supply-chain security.

Uranium – Demand underpinned by policy support and rising demand for nuclear energy.

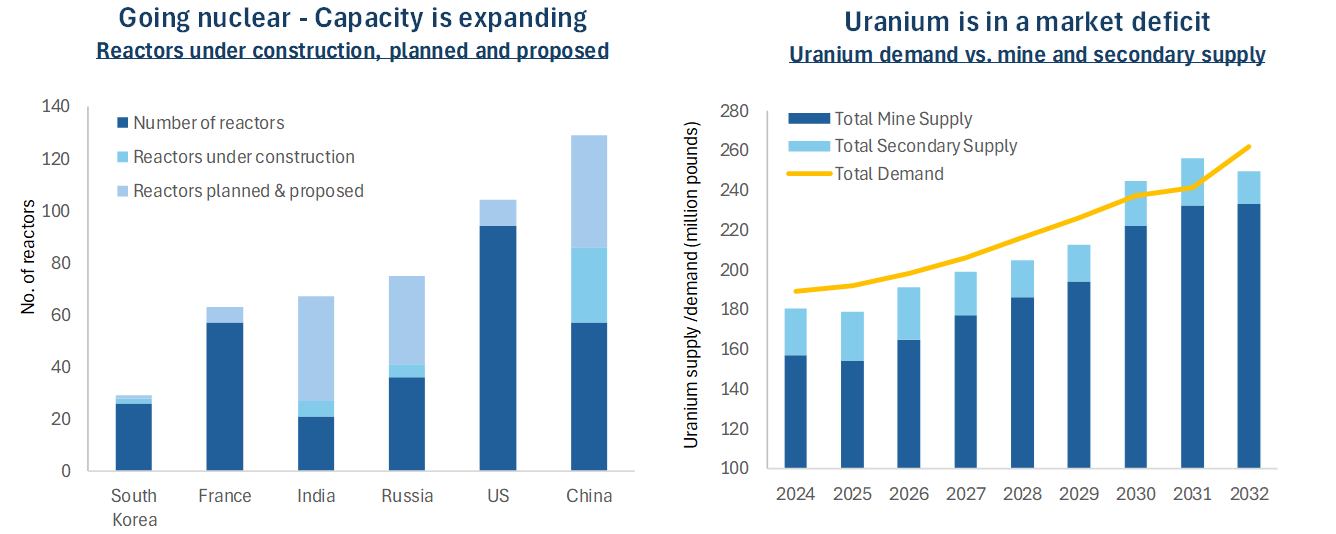

We now turn to the uranium sector, which has seen its fortunes shift dramatically in recent years as nuclear energy has enjoyed a renaissance of support, both from governments and the private sector. Uranium demand is forecast to rise 39% by 2030[xvi], driven by decarbonisation and energy security objectives that are extending the lifetimes of existing reactors, enabling the restart of offline reactors, and supporting a new wave of reactor builds, both large-scale plants and small modular reactors (“SMR”). Nuclear capacity is once again expanding, led by China, India, and Russia, alongside renewed policy support in the US. In Europe, policy sentiment has also shifted, with Sweden’s parliament voting this month to lift its uranium mining ban from 2026, and with countries including France, Belgium and the Netherlands implementing or considering reactor lifetime extensions and new builds.

On the supply side, the uranium market remains constrained after more than a decade of underinvestment, during which mines were shuttered and new projects faced lengthy permitting processes. As shown in the chart below, the market is currently in deficit, relying on secondary supply to fill a 30-40mlb annual shortfall. These secondary sources, from inventory drawdowns and strategic stockpiles, are finite and cannot indefinitely compensate for rising demand and limited primary production[xvii].

Figure 5

Source: World Nuclear Association, UxC, TD Cowan.

Public perception of nuclear power has improved markedly in recent years, driven by growing recognition of its role as a source of clean, reliable baseload power and its importance for energy security. This shift has translated into stronger policy support. Under the Biden Administration, the 2022 Inflation Reduction Act introduced incentives for existing and new nuclear capacity. This momentum has accelerated under President Trump, who has issued a series of executive orders aimed at stimulating nuclear sector growth. Current targets include deploying 300GW of net new nuclear capacity by 2050 and having 10 large reactors under construction in the US by 2030[xviii].

To advance these goals, the US government announced a landmark partnership last month with the owners of Westinghouse Electric, committing at least USD 80 billion to new reactor construction[xix]. Under this agreement, the government will arrange financing and support permitting for new reactors. Such political support is critical given the last two Westinghouse reactors built in Georgia in 2023 and 2024 were delivered around seven years behind schedule and cost around double the original estimate of USD 14 billion[xx].

On the private sector side, major US technology companies are increasingly funding SMR development to secure clean, reliable power for their rapidly expanding AI and data centre operations. Google has signed agreements with US nuclear providers to develop advanced SMRs in the Southeast US, targeting around 500MW by the mid-2030s, in what has been described as the first large-scale corporate nuclear procurement of its kind[xxi]. Amazon has undertaken c.USD 700 million of investment aimed at deploying SMRs for its data centres[xxii], while Microsoft has signed long term nuclear power purchase agreements (“PPA”) and continues to signal active interest in SMR technologies[xxiii].

With Western nuclear energy now entering a new growth cycle after years of stagnation, we see both opportunities and challenges for investors. On the one hand, uranium supply is unlikely to keep pace with rising demand without a meaningful increase in price, while potential bottlenecks in enrichment may limit growth in nuclear capacity. The re-stocking cycle will likely prove a favourable catalyst for uranium prices as utility companies, which have been drawing down uranium stocks, look to replenish. Furthermore, recent indications of production curtailments from Cameco and Kazatomprom, the world’s two largest uranium miners, have supported pricing. We continue to see upside potential given the prospect of a deepening market deficit heading into 2026, though volatility is likely as new supply announcements emerge. Baker Steel’s Electrum strategy has maintained tactical exposure to uranium in recent years, to the benefit of our investors. We continue to emphasise the importance of active stock selection and agile asset allocation in navigating this highly specialised and rapidly evolving sector.

Lithium – Oversold and oversupplied, are we near a turning point?

No discussion of critical minerals is complete without addressing lithium. Central to modern battery technology, lithium underpins a wide range of green industries, making secure supply essential for continued technological growth. Demand for lithium is forecast to rise 147% by 2030[xxiv], putting it amongst the metals with the fastest growing consumption. Its role is indispensable in powering EV batteries, grid-storage systems, and in consumer electronics, placing it at the core of global electrification.

Notably, energy storage systems (“ESS”), which currently represent around 20% of global lithium demand, are forecast to grow in prominence as a driver of lithium demand. Between today and 2030, global ESS are forecast to grow by around 21% annually, representing a rapid expansion of installations to support the growth of energy demand and renewable energy capacity[xxv]. The adoption of AI is likely to exacerbate this growth, as AI data centres create grid stress and accelerate ESS requirements.

Prices surged in 2022 as the Inflation Reduction Act and other international Net Zero policies accelerated demand. Today lithium prices have corrected sharply from their 2022 highs, yet long-term fundamentals remain robust. EV adoption continues to grow, albeit more moderately than previously projected. In 2024, global EV sales increased by 3.5m units, exceeding the entire global total for 2020[xxvi]. EVs represented 20% of all cars sold in 2024, with sales surpassing 17 million vehicles[xxvii]. In response to the strategic importance of securing supply, major automakers are locking in long-term offtake agreements, while Western governments push to build domestic battery-metal supply chains. This strategic importance was underscored in October 2025, when Lithium Americas secured a USD 2.23 billion loan from the US Department of Defence.

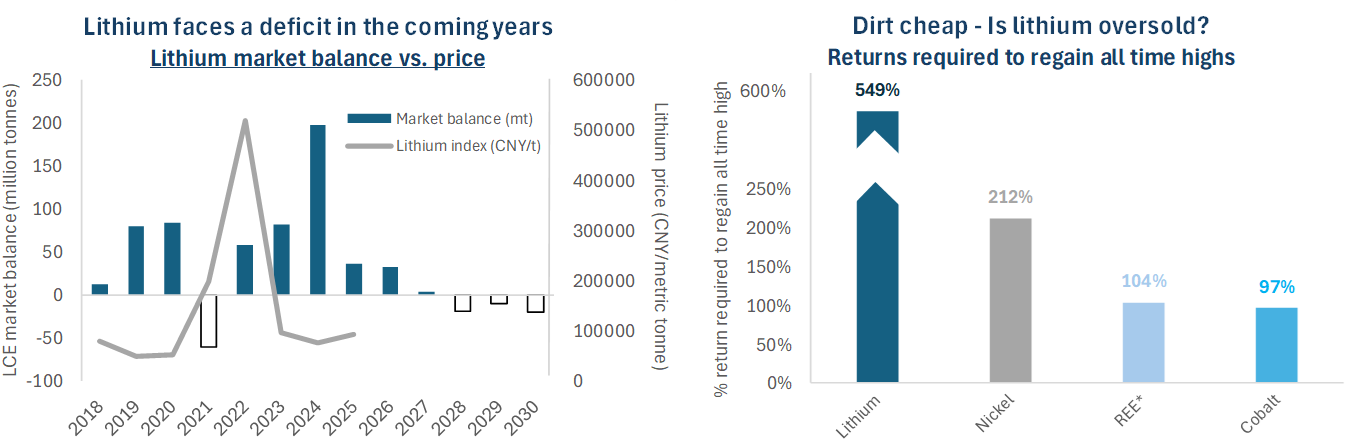

Figure 6

Source: NBC, Bloomberg. Data as at 14th November 2025. All data in USD terms. Note, LCE is Lithium Carbonate Equivalent. *REE refers to NdPr.

Today, however, the lithium market is in surplus, following an expansion of supply in recent years. Significant new volumes have come online, from hard rock spodumene expansions in Australia, to brine developments in Chile and Argentina, and rapid output growth from China’s lepidolite and brine operations. This wave of new supply, combined with a deceleration in EV sales growth, has driven lithium prices lower. The surplus has been reinforced by Chinese producers and refiners continuing to operate at extremely low margins to protect market share. Lithium may now be one of the most oversold metals and would need to recover by c.580% to regain its 2022 peak[xxviii]. As shown in the chart above, this surplus is expected to persist into next year before the market moves back into deficit in 2027/2028.

After two years of weak performance, lithium prices are now showing early signs of recovery, supported by optimism around rising demand from grid-scale battery storage, with prices up 25% year-to-date[xxix]. This aligns with our view that the sector retains a strong long-term outlook, despite near-term volatility. We view lithium’s surplus as cyclical rather than structural, making it a temporary imbalance. As with many critical minerals, bringing new lithium projects into production remains a lengthy and capital-intensive process.

We are also seeing evidence of strategic production curtailments by lithium producers, which may accelerate the market’s tightening. In August 2025, CATL (Contemporary Amperex Technology Co) temporarily suspended 46kt of LCE capacity, equivalent to roughly 3% of global 2025 supply[xxx]. Meanwhile, Albemarle, the world’s largest lithium producer, announced the mothballing of its Chengdu lithium-hydroxide plant and the delay or cancellation of several expansion projects[xxxi]. These cuts represent meaningful volumes and could pull the market back toward deficit sooner than expected, particularly if more producers follow suit. The sector’s recent rally also underscores how quickly sentiment and fundamentals can shift when demand accelerates, such as through stronger grid-storage deployment or a potential reacceleration in EV sales. A future restocking cycle, following the drawdown of inventories over the past two years, would present an additional catalyst for recovery.

Active investment management in a highly specialised sector

Critical metals industries face a transformative period ahead, as technological development drives demand and supply challenges persist. The opportunities for investors in the mining sector are substantial and varied, from the well-known metals discussed in this report, to the lesser-known metals with vital applications in technology. From gallium and germanium, required for semiconductors and other sensitive technologies, to titanium and tungsten, key metals in aerospace and defence, each of which has its own distinct demand and supply dynamics, yet are all shaped by the broader forces of accelerating technological adoption and growing strategic pressure on global supply chains. Given this complexity, we believe that active investment management is the most appropriate approach for navigating this highly specialised sector.

In this report, we have focused on REEs, uranium, and lithium; all metals which Baker Steel’s Electrum strategy has held meaningful exposure to in recent years, alongside producers of other critical metals including copper, aluminium, silver and gold. Given the dynamic nature of the sector, profit-taking and rotation between sub-sectors is undertaken actively. As a leading natural-resources fund manager, Baker Steel’s aims to offer nimble exposure to the producers of the critical raw materials underpinning the New Industrial Revolution, with a value-driven ethos. Our investment process combines bottom-up equity analysis, assessing asset quality, operational performance, and risk exposure, with top-down insights into commodity trends, geopolitical developments, and structural demand drivers.

Looking ahead, we believe the current wave of rapid technological change, powered by AI, robotics, electrification and clean energy, is transforming global metals demand. A potent combination of pro-growth industrial policy, metals-intensive innovation, and structurally tight raw-material supply chains provides a compelling backdrop for a sustained period of strength in the mining and critical minerals sectors.

[i] USGS

[ii] Canaccord

[iii] Canaccord

[iv] BMO

[v] Global Wind Energy Council

[vi] Source: AI Insight Media, Trafigura, Reuters, Microsoft, BMO, Ivanhoe Mines, Baker Steel internal

[vii] Arafura Resources, using Adamas and Project Blue data

[viii] MP Materials

[ix] Pensana PLC

[x] Vulcan Elements

[xi] Reuters

[xii] Neo Performance Materials

[xiii] Japan Organisation for Metals and Energy Security (JOGMEC)

[xiv] BMO

[xv] CNBC

[xvi] TD Cowen, 2024-2030 forecast

[xvii] International Atomic Energy Agency

[xviii] World Nuclear Association; Utility Dive

[xix] Reuters

[xx] Reuters

[xxi] Reuters

[xxii] World Nuclear News

[xxiii] TechRadar

[xxiv] Scotia, 2024-2030 forecast

[xxv] BloombergNEF

[xxvi] IEA

[xxvii] IEA

[xxviii] Bloomberg, in USD terms

[xxix] Bloomberg, China Lithium Carbonate, in USD terms

[xxx] Reuters

[xxxi] The Australian

About Baker Steel Capital Managers LLP

About Baker Steel Capital Managers LLP

Baker Steel Capital Managers LLP manages three award winning investment strategies, covering precious metals equities, speciality metals equities and diversified mining.

Baker Steel has a strong track record of outperformance relative to its peers and relative to passive investments in the metals and mining sector. BAKERSTEEL Precious Metals Fund is the 2025 winner of the GELD-Magazin Alternative Investment Award, and 2025 winner for the seventh year running of the Lipper Fund Awards while BAKERSTEEL Electrum Fund is the 2025 winner of the Euro Fund Awards Commodity Equities Performance over 10 years. The Baker Steel Resources Trust has also been named Investment Company of the Year 2021, 2020, 2019, Natural Resources, by Investment Week.

Fund Managers Mark Burridge and David Baker have been awarded two Sauren Gold Medals for 2021 and were awarded Fund Manager of the Year at the 2019 Mines & Money Awards.

Important

Please Note: This document is a financial promotion is issued by Baker Steel Capital Managers LLP (a limited liability partnership registered in England, No. OC301191 and authorised and regulated by the Financial Conduct Authority) for the information of a limited number of institutional investors (as defined in the Fund prospectus) on a confidential basis solely for the use of the person to whom it has been addressed. This document does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe or purchase any shares or any other interests nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefor. Recipients of this document who intend to apply for shares or interests in Baker Steel’s funds are reminded that any such application may be made solely on the basis of the information and opinions contained in the relevant prospectus or other offering document relating thereto, which may be different from the information and opinions contained in this document. This report may not be reproduced or provided to any other person and any other person should not rely upon the contents. The distribution of this information does not constitute or form part of any offer to participate in any investment. This report does not purport to give investment advice in any way. Past performance should not be relied upon as an indication of future performance. Future performance may be materially worse than past performance and may cause substantial or total loss.