The competition for critical minerals is heating up

Metals have become strategic again. How can investors benefit?

Commodity markets have entered an era in which metals and minerals are no longer simply economic inputs but critical strategic assets. The pricing and availability of raw materials is increasingly shaped by geopolitics and industrial policy, alongside macroeconomic forces. Recent global shocks, most notably the ongoing Middle Eastern conflict, have brought supply chain vulnerabilities into sharp focus. From key industrial metals, such as copper and aluminium, to speciality metals such as lithium, uranium, and rare earth elements (“REE”) security of supply is a challenge.

Miners lie at the heart of the competition for critical minerals and offer investors effective exposure to the secular demand trends for commodities from new technology, energy production and security in an increasingly multi-polar world. Furthermore, an increasingly supportive macroeconomic backdrop is evolving for hard assets, including metals and miners, characterised by persistent inflation globally, potential fiscal dominance in the West, and long-term de-dollarisation. Against this backdrop gold has restored its role as a reserve asset.

Metals and mining have never been more relevant for investors –

- Strategic capital is flowing into the mining sector as the US and other Western governments ramp up financing and investment in supply chains for critical raw materials.

- Stockpiling, tariffs and export controls for critical minerals reflect the strategic importance of metals and the risk of shortages.

- Supply deficits are forecast for many critical metals, as secular demand growth from technology and energy security meets constrained supply.

- Mining equities are under-owned and appear undervalued despite strong margins, cost management and capital discipline.

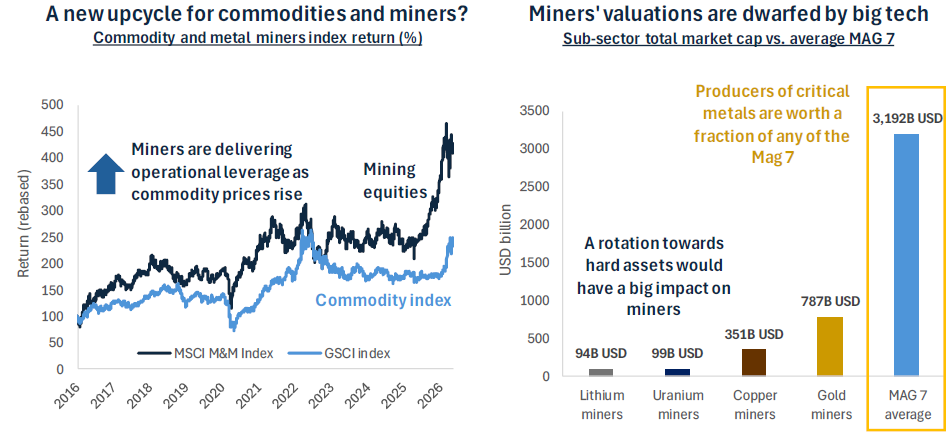

Figure 1

Source: Bloomberg, Baker Steel internal. Data as at 7th May 2026.

Conflict and commodities – Strategic interests are focused on critical metals

As the world’s demand for critical metals and minerals continues to grow, so too does their strategic importance for governments seeking economic growth, technological leadership and national security advantages. Metals are benefiting from a range of powerful structural demand trends, from the expansion of artificial intelligence and data infrastructure to the clean energy transition, electric vehicle (“EV”) adoption, renewable power generation and grid scale energy storage.

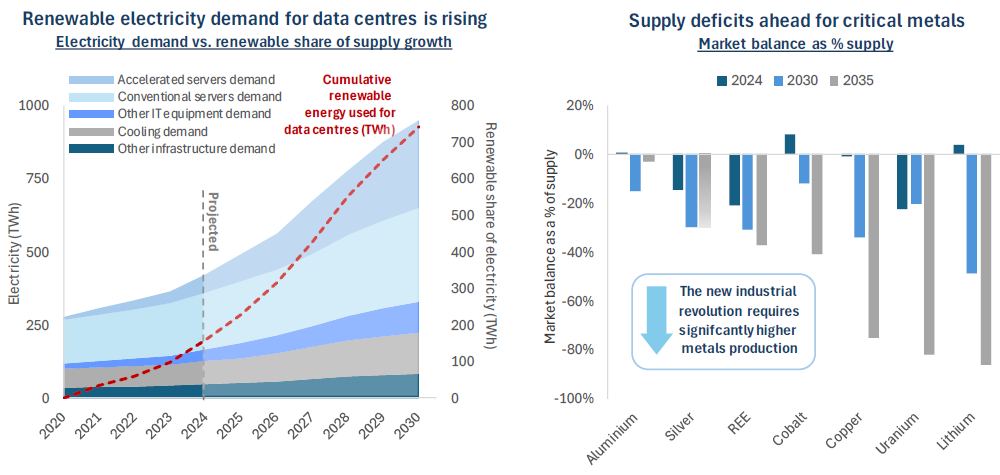

Electrification lies at the centre of this demand story across a wide range of industries. As emerging technologies account for an increasing share of global economic activity, demand for electricity, particularly clean energy, is expected to rise steadily. As shown on the chart below, AI data centres present a prime example of this trend, requiring rapid energy supply growth from renewables. This is driving a profound shift in the strategic importance of metals. It is estimated that Chinese demand for copper and aluminium from clean technology applications will surpass demand from domestic construction this year[i]. More broadly, by 2035 copper demand is forecast to increase by 29%, aluminium by 23%, lithium by 307% and uranium by 29%, alongside a range of other metals with strong long term demand outlooks[ii]. As illustrated in the chart below, these powerful demand trends, combined with growing supply side constraints, point towards substantial future deficits across several critical metals markets.

The ongoing conflict in the Middle East has further highlighted the strategic role of metals in areas ranging from energy security to defence. The US government is estimated to have spent approximately USD 11.3 billion during the first week of the conflict alone[iii]. Modern defence systems are highly metals intensive, requiring copper for electronics, tungsten for munitions, nickel for aerospace applications and rare earth magnets for advanced guidance systems. The replenishment of munitions is also increasingly expensive, particularly as interceptor missiles costing millions of dollars are deployed against comparatively low cost drones. More broadly, the conflict has intensified the strategic focus on supply chain security, with multi year defence procurement programmes now being expanded across the world.

Figure 2

Source: USGS, IEA, Baker Steel internal, International Aluminium Institute.

Supply risks for critical metals span a wide range of factors, including technical, geological, operational and permitting challenges. In recent years, however, geopolitical risk has become increasingly prominent. Strategic competition between major powers has brought industrial policy, resource control and supply chain security to the forefront of economic and political decision making. The conflict in the Middle East has further exposed the fragility of global supply chains and the vulnerability of key trade chokepoints, while also underscoring the importance of input costs across raw materials markets.

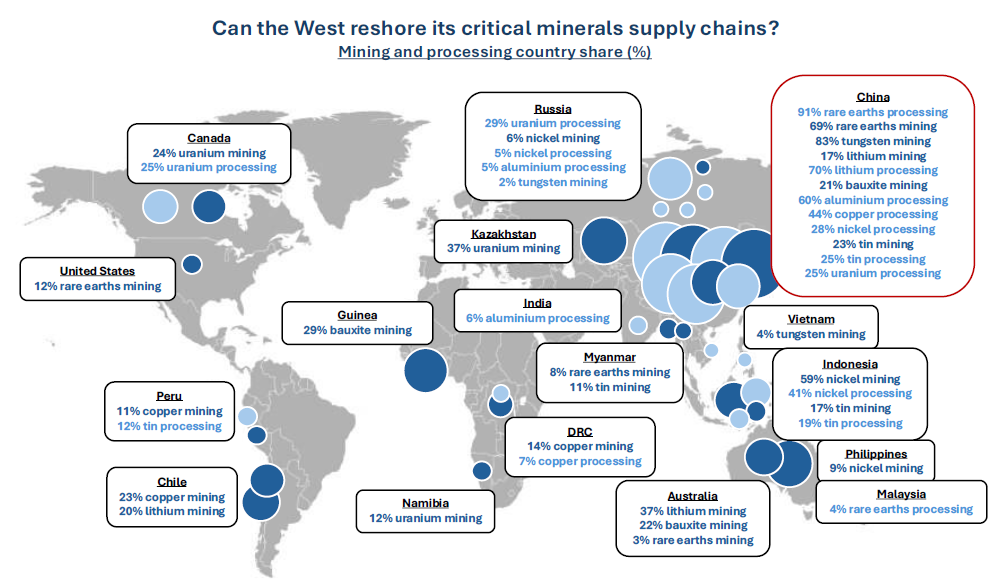

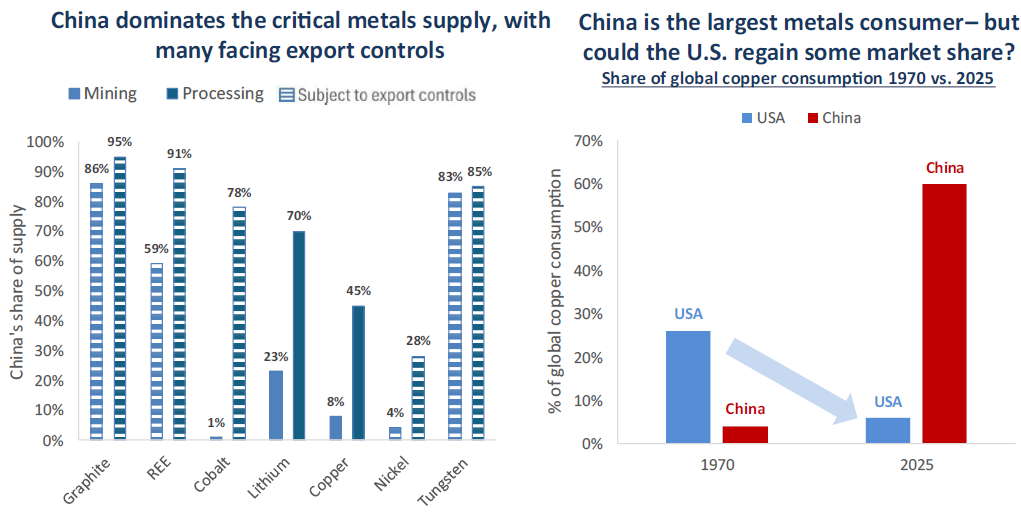

Metals production depends heavily on energy, chemicals and logistics, all of which are now subject to heightened volatility and constraint. At the same time, metals supply chains remain highly globalised, yet concentrated in a relatively small number of countries and regions that possess either substantial mineral reserves or dominant processing capacity. As illustrated in the graphic below, China’s dominance across both production and processing, combined with the vulnerability of critical shipping routes and rising trade tensions, presents a compelling case for Western nations to reshore and secure supply chains for critical raw materials.

Figure 3

Source: USGS, IEA, World Nuclear Association, International Institute for Sustainable Development, International Tin Association, Baker Steel internal. Data as at 12th May 2026.

As a result, recent years have seen a marked shift towards interventionist strategic policies, combining subsidies, loans, equity stakes and diplomatic agreements to secure critical mineral supply chains. The United States has led this transition through an unprecedented mobilisation of capital and policy support aimed at strengthening domestic and allied critical mineral supply.

On the policy front, this has involved both new legislation and the repurposing of existing frameworks. Under the Biden administration, the Inflation Reduction Act (“IRA”) of 2022 represented a major expansion of funding for clean energy and strategic supply chains. Although parts of the legislation were later rolled back under the Trump administration, key measures including advanced manufacturing production credits, subsidies and domestic content requirements remain central to the broader strategic effort to reduce dependence on China[iv].

Under President Trump, the development of critical minerals policy has accelerated further through deregulation, streamlined mining approvals and the introduction of the One Big Beautiful Bill Act (“OBBBA”). For the first time, the OBBBA explicitly allocates substantial federal funding towards critical mineral extraction, processing, refining and associated infrastructure. The legislation provides for up to USD 5 billion of direct investment into the critical minerals supply chain, alongside USD 500 million in credit subsidies supporting up to USD 100 billion in loan guarantees for critical mineral projects. In addition, the Act allocates USD 3.3 billion to support offtake agreements and strategic purchasing within the critical minerals sector[v]. Complementing these measures, Project Vault aims to establish a USD 12 billion strategic national reserve of critical minerals, including rare earths, lithium and nickel.

At the same time, several existing policy frameworks have been repositioned to support critical mineral supply chains. The Defense Production Act has become a major source of financing for critical minerals projects, while the US Export Import Bank has been directed to provide financing for the sector. Similarly, the US International Development Finance Corporation (“DFC”) is extending large scale loans to overseas mining projects, while substantial funding packages under the CHIPS Act have also been directed towards critical minerals initiatives[vi].

The Trump 2.0 administration is estimated to have committed approximately USD 18.6 billion to the critical minerals sector across around 60 projects to date[vii]. The scale of US government support for mining companies is particularly notable. Lithium Americas’ Thacker Pass project in Nevada, initially supported by a USD 2.26 billion Department of Energy (“DOE”) loan in 2024, has subsequently evolved into a direct equity participation by the US government alongside a joint venture with General Motors. This represents a significant departure from previous policy, with Washington now co investing directly to secure domestic lithium supply rather than simply financing projects[viii].

A similar approach can be seen with MP Materials, operator of Mountain Pass, the only active REE mine in the United States. The US Department of Defense supported the company through financing and a strategic investment valued at USD 550 million[ix]. The transaction reflects the strategic importance of REEs for defence technologies and electric vehicles, as well as the broader US objective of reducing China’s dominance across critical mineral supply chains.

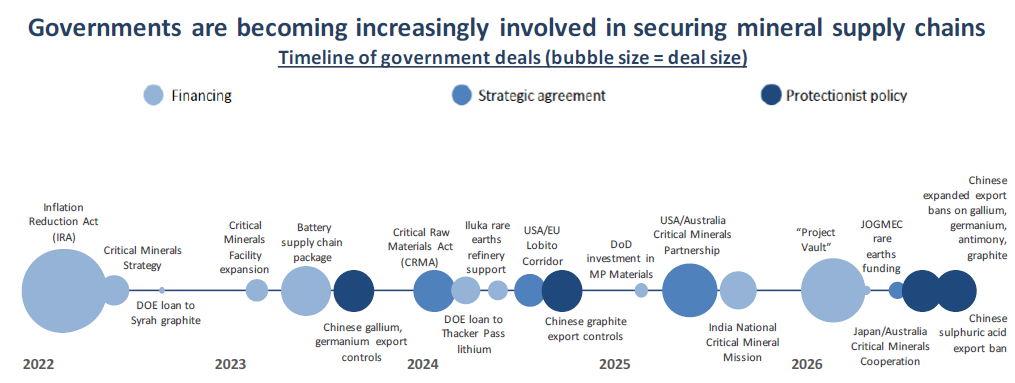

Figure 4

Source: Company disclosures, DoE, DoD.

Outside the United States, Western governments are also implementing policies aimed at strengthening the resilience of critical mineral supply chains. Pax Silica, a US-led strategic initiative, seeks to establish a USD 1 trillion Western aligned AI supply chain incorporating the relevant critical minerals required to support advanced technologies. Similarly, the US-Australia Critical Minerals Partnership, signed in 2025, deepens cooperation on supply chains for lithium, rare earths and other strategic minerals, with an estimated USD 8.5 billion in project financing available to reduce dependence on China[x].

In Europe, France, Germany and Italy are leading a coordinated effort to establish joint stockpiles across the bloc. RESourceEU is focused on creating a “Critical Raw Materials Centre” to monitor, jointly procure and stockpile materials such as battery raw materials and permanent magnets[xi]. The UK is also exploring stockpiling initiatives through NATO cooperation and domestic resilience focused policy frameworks. India is similarly developing strategic reserves for rare earths, while Japan and South Korea have already established government managed stockpiling systems.

Despite these initiatives, questions remain as to whether such efforts will be sufficient to counter China’s dominance of critical metals markets. As the world’s leading producer and processor, China maintains significant control over supply chains and has emerged as the most prominent user of export controls on critical metals and minerals as a strategic policy tool. In recent years, China has imposed restrictions on exports of gallium and germanium, both essential inputs for semiconductors and defence technologies, while also tightening controls on graphite, a critical material for lithium-ion batteries.

There are important historical precedents for such actions. China’s restrictions on rare earth exports during the 2010s disrupted global markets and prompted countries including the United States, Japan and Australia to accelerate efforts to diversify supply chains. More recently, since November last year China has placed export restrictions on a range of processing equipment, and has signalled the potential introduction of controls on rare earth processing technologies, highlighting the extent of its leverage across the critical minerals value chain.

Figure 5

Source: IEA, USGS.

As risks to mineral supply chains mount and governments seek to protect strategic industries from market shocks, the implications for the metals and mining sector are stark. Inflationary pressure, potential shortages, and higher commodity prices are possible, alongside a greater focus on the mining industry by both policymakers and investors.

Conflict in the Middle East – Can miners manage global shocks and rising input costs?

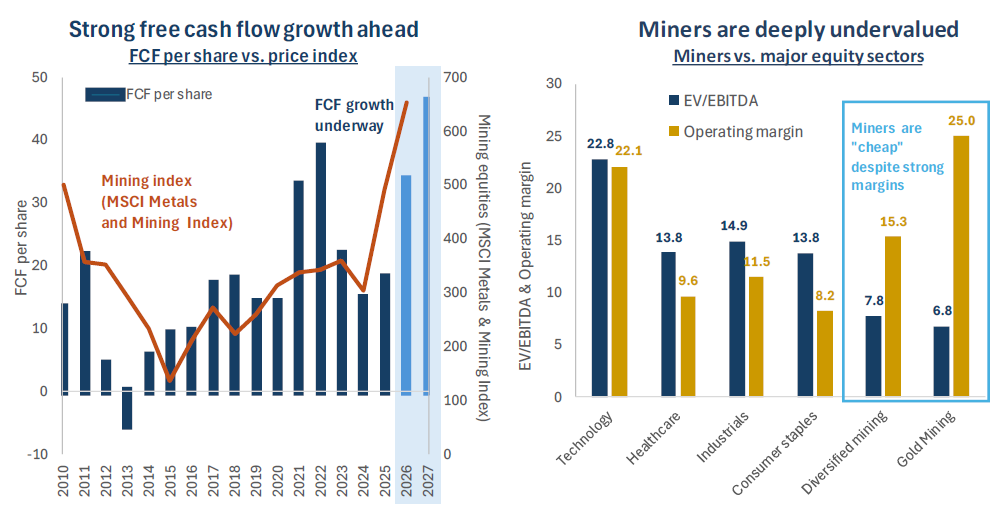

Mining companies sit at the centre of the global race for critical minerals, bringing the sector back into focus for investors for the first time in many years. Despite this growing strategic importance, the sector remains deeply under-owned, with mining equities accounting for just 0.4% of global equity markets[xii]. However, capital is beginning to return to the sector. Assets in mining ETFs have more than doubled over the past year to USD 87.4 billion, while inflows reached USD 8.2 billion during Q1, reversing the outflows experienced in 2025[xiii]. Furthermore, analyst coverage of the mining sector also appears to be increasing, with several large banks including J.P. Morgan, Goldman Sachs, Bank of America, UBS and HSBC recently publishing more visible commodities coverage, especially around metals and energy transition themes[xiv].

This trend is consistent with a broader investor rotation towards hard assets, and we expect interest in the mining sector to continue increasing as structurally stronger demand trends gather momentum. As illustrated in the charts below, mining companies continue to demonstrate strong cash generation, which has been an important driver of share price performance over the past year. Importantly, despite the recent recovery in valuations, the mining sector still appears significantly undervalued relative to broader equity markets.

Figure 6

Source: Bloomberg.

The current conflict in the Middle East has wide ranging implications for the mining sector. Disruptions to the Strait of Hormuz have affected global energy flows, creating knock on effects across fertiliser markets, sulphur supply chains and other industrial inputs. For metals markets, the result has been rising cost pressures and growing physical bottlenecks.

In terms of the direct impact on mining companies, fuel costs typically account for around 10% of operating costs. For gold miners, it is estimated that every USD 10 increase in the oil price adds approximately USD 10/oz to operating costs[xv]. Copper miners may meanwhile face an increase of approximately USD 0.17/lb in C1 operating cost inputs for every USD 10 rise in oil prices[xvi].

Given the varying impact across different subsectors, copper provides a useful starting point. While the market has not yet experienced a large scale loss of primary supply, it is being squeezed through its dependence on industrial inputs. Sulphuric acid, which is essential for copper leaching, has experienced significant price inflation as sulphur supply has tightened. Sulphuric acid can account for up to 30% of operating costs for copper projects utilising Solvent Extraction and Electrowinning (“SX EW”) processing. These conflict related cost pressures come on top of already challenging supply side conditions for copper. Ore grades continue to decline, while new projects now require nearly 18 years to reach production, compared with 12.7 years in the mid 2000s[xvii]. The copper sector is increasingly constrained not only by geology, but also by permitting challenges, input costs and operational complexity, creating an environment in which rising demand is meeting constrained supply.

Aluminium is even more directly exposed to rising input costs, given its highly energy intensive production process and cost structure closely linked to electricity prices. A significant proportion of global aluminium supply is concentrated in the Gulf region, with around 9% of global primary aluminium smelting capacity located there and approximately 75 to 80% of that output passing through the Strait of Hormuz. The recent conflict has placed several million tonnes of production at risk while simultaneously increasing energy costs, contributing to higher aluminium prices. Aluminium also illustrates how active management can benefit investors during periods of crisis.

Beyond the direct impact on industrial metals, a range of energy related metals also appear well supported as conflict in the Middle East, together with broader concerns over energy security, strengthens the case for renewable and nuclear energy. The uranium sector, in particular, is benefiting from accelerating support for nuclear power as a reliable source of baseload energy. In a world characterised by volatile oil prices, supply risks and rising electrification demand, energy security has become increasingly important for policymakers. Rising uranium demand is occurring against a backdrop of constrained supply following years of underinvestment and lengthy development timelines.

Lithium, a key metal for battery technology and the energy transition, has also benefited from a price recovery in recent months following weakness caused by oversupply. While still facing a supply surplus, lithium appears to offer strong long-term prospects, supported by firm energy storage solutions (“ESS”) demand and supply disruptions in China and Zimbabwe. CRU expects prices could rise towards USD 28/kg in the near term, although overall the lithium price would still need to rise by more than 257% to regain its all-time highs[xviii].

As active investors in the mining sector, Baker Steel has traded tactically around these themes since the onset of the conflict. At the core of our investment thesis is the renewed focus on critical mineral supply chains and the recognition that metals have become strategic once again.

The macro picture – Debt, De-Dollarisation, and the Case for Precious Metals

The strategic themes discussed throughout this report have focused primarily on the metals and minerals essential to technology, industry and defence. Precious metals also form an important part of this landscape, particularly silver and platinum, which benefit from growing industrial and technological demand. Beyond these sector-specific drivers, however, a broader set of macroeconomic forces is creating an increasingly supportive backdrop for precious metals more generally, with strategic allocations to gold by both central banks and investors continuing to rise. There are also signs that China is likely stockpiling more silver for strategic and industrial reasons, resulting in market tightening[xix].

Gold’s response to recent geopolitical events has been consistent with its long-established role as a store of value and safe-haven asset. Periods of heightened geopolitical tension and uncertainty tend to support demand, although episodes of liquidity-driven selling and profit-taking can still lead to short-term weakness. This was evident in March, when gold briefly sold off amid a knee-jerk market reaction to uncertainty surrounding the direction of monetary policy. Nevertheless, the longer-term macroeconomic drivers underpinning gold continue to strengthen.

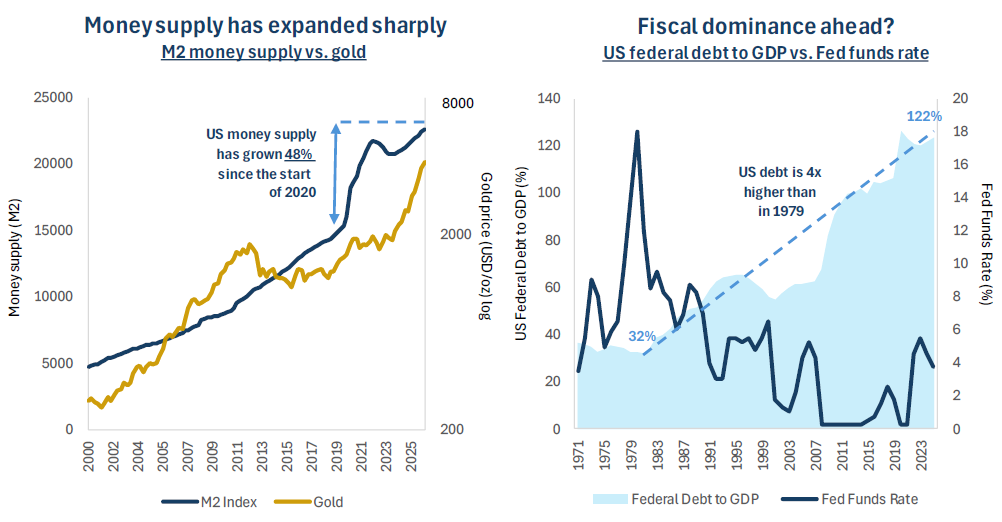

Macroeconomic conditions are currently characterised by rising inflationary pressures and a weakening US fiscal position, against a backdrop of elevated sovereign debt levels and increasing reliance on fiscal policy. The US now faces annual debt servicing costs exceeding USD 1 trillion, representing approximately 19% of federal revenues, more than is spent on defence. The recent conflict in the Middle East is adding further pressure to fiscal deficits, while the longer-term trend of de-dollarisation continues as central banks diversify reserve holdings.

Figure 7

Source: Bloomberg. Data as at 31 March 2026.

Inflationary pressures are also intensifying as a result of the ongoing energy crisis linked to conflict in the Middle East, although inflationary forces were already building due to tariff policies and the extraordinary levels of monetary expansion following the COVID pandemic. As illustrated in the chart above, money supply (M2) has expanded by 48% since the beginning of 2020, meaning that approximately one-third of all US dollars currently in circulation have been created during this relatively short period[xx]. Stagflation also presents as a potential outcome as risks to economic growth rise, exacerbated by the Middle Eastern conflict.

Against a backdrop of high debt levels and persistent inflation, we view fiscal dominance as an increasingly likely outcome, with central banks facing mounting pressure to maintain low interest rates and continue monetary expansion in support of economic growth. In an environment where nominal yields remain below inflation, currencies are gradually debased and the real burden of debt is reduced over time. For investors, this form of financial repression strengthens the case for holding real assets, particularly precious metals, alongside scarce assets such as industrial and specialty metals, and equities linked to real cash flows.

As the US economic environment increasingly exhibits characteristics of fiscal dominance and financial repression, combined with the ongoing transition away from a unipolar currency system, we believe the strategic role of precious metals is becoming ever more significant. In this context, gold is no longer simply an inflation hedge or crisis asset; it is increasingly re-emerging as a core monetary asset within a more fragmented global financial system.

Metals have become strategic again

The global race for critical minerals is already underway. Recent shocks driven by conflict, geopolitical tension and rapid technological change have sharpened the focus on securing resilient supply chains. Looking ahead, we expect strategic considerations to become an increasingly important force shaping the metals and mining sector, creating compelling opportunities for investors in what remains an under-owned area of the market.

In our view, the market continues to underestimate both the longevity and the strategic importance of the current commodity cycle. Following more than a decade of underinvestment, supply constraints across a range of key metals are beginning to emerge just as demand accelerates, driven by electrification, AI infrastructure, power grid expansion and intensifying geopolitical competition for secure resource access. In this environment, metals have regained strategic significance.

At the same time, persistent fiscal deficits, elevated sovereign risk and the prospect of structurally lower real interest rates continue to reinforce the investment case for gold and other hard assets. Taken together, we believe these dynamics create a highly supportive backdrop for active management and selective investment across the metals and mining sector.

[i] CRU

[ii] USGS, IEA, Baker Steel internal, International Aluminium Institute

[iii] CBS

[iv] US Treasury / IRS

[v] BMO Capital Markets

[vi] BMO Capital Markets

[vii] BMO Capital Markets, as at 11 May 2026.

[viii] Lithium Americas

[ix] MP Materials

[x] Australian Government (Department of Industry, Science and Resources)

[xi] RESourceEU

[xii] MSCI, Reuters

[xiii] ETFGI, Reuters, data at Q1 2026

[xiv] JPMorgan Chase

[xv] Newmont

[xvi] Capstone

[xvii] S&P Global Commodity Insights

[xviii] Bloomberg. Data as at 30 April 2026

[xix] Kitco News

[xx] Bloomberg

About Baker Steel Capital Managers LLP

About Baker Steel Capital Managers LLP

Baker Steel Capital Managers LLP manages three award winning investment strategies, covering precious metals equities, speciality metals equities and diversified mining.

Baker Steel has a strong track record of outperformance relative to its peers and relative to passive investments in the metals and mining sector. BAKERSTEEL Precious Metals Fund is the 2025 winner of the GELD-Magazin Alternative Investment Award, and 2025 winner for the seventh year running of the Lipper Fund Awards while BAKERSTEEL Electrum Fund is the 2025 winner of the Euro Fund Awards Commodity Equities Performance over 10 years. The Baker Steel Resources Trust has also been named Investment Company of the Year 2021, 2020, 2019, Natural Resources, by Investment Week.

Fund Managers Mark Burridge and David Baker have been awarded two Sauren Gold Medals for 2021 and were awarded Fund Manager of the Year at the 2019 Mines & Money Awards.

Important

Please Note: This document is a financial promotion is issued by Baker Steel Capital Managers LLP (a limited liability partnership registered in England, No. OC301191 and authorised and regulated by the Financial Conduct Authority) for the information of a limited number of institutional investors (as defined in the Fund prospectus) on a confidential basis solely for the use of the person to whom it has been addressed. This document does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe or purchase any shares or any other interests nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefor. Recipients of this document who intend to apply for shares or interests in Baker Steel’s funds are reminded that any such application may be made solely on the basis of the information and opinions contained in the relevant prospectus or other offering document relating thereto, which may be different from the information and opinions contained in this document. This report may not be reproduced or provided to any other person and any other person should not rely upon the contents. The distribution of this information does not constitute or form part of any offer to participate in any investment. This report does not purport to give investment advice in any way. Past performance should not be relied upon as an indication of future performance. Future performance may be materially worse than past performance and may cause substantial or total loss.