A new wave of M&A deals is underway in the mining sector as companies seek to grow production in the face of CAPEX inflation and long permitting timelines. The gold and lithium sectors are leading the way in terms of deal making. In the gold space this is driven by potential value and synergy opportunities, while in the lithium space, it is driven by prospects of rapid long-term growth in a sector where size matters, as battery consumers look for scalable supply. Newmont Mining’s proposal to acquire Newcrest Mining last month, while rejected, highlights the rising interest in M&A in the gold sector, which comes as gold miners remain undervalued relative to historic levels. Gold miners are in the strongest financial shape that they have been in for years, offering robust margins and paying shareholder returns.

Meanwhile, lithium producers face a transformation in the years ahead as battery production ramps up to meet surging demand for electric vehicles (“EVs”) and green technology. Prices of lithium, a key battery metal, have risen rapidly in recent years and lithium assets are increasingly of interest both to diversified mining companies seeking to increase production of this critical metal, and to car manufacturers themselves, seeking to secure their own supply chains. As long-term value investors focused on the metals and mining sector, we consider that the current wave of M&A is likely to continue and presents attractive opportunities for investors:

Cheaper to buy than build – M&A a solution to capital cost inflation, permitting delays, and supply chain issues.

Unlocking value – Active stock selection is key to invest in companies well-placed to benefit from M&A.

New entrants – Manufacturers, energy companies and other new entrants are seeking to secure supply.

Size matters – Gold companies seek to extract synergies, while lithium producers seek scale.

Discipline – Unlike previous periods of M&A, the current wave of deals appears disciplined and value accretive.

Macroeconomic conditions favour miners – Real interest rates are likely to weaken, amid elevated inflation.

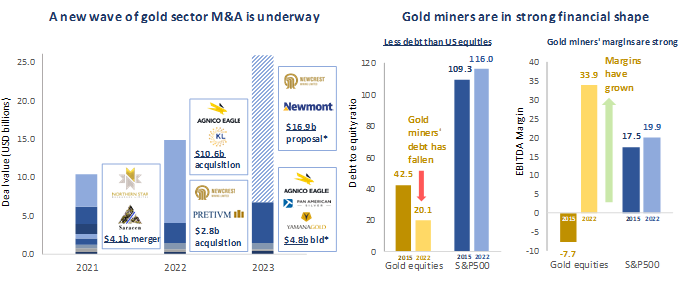

Dealmaking among gold majors is gaining pace, amid improving financial health for the sector. Gold miners compare favourably relative to broader equities in terms of margins and debt, having recovered strongly since the lows of 2015.

Figure 1

Source: Bloomberg, Baker Steel Capital Managers LLP. Note, based on completion date. *Pendingcompletion, Newcrest offer rejected.

New gold sector M&A highlights miners’ profitability and undervaluation

Given the gold sector’s relative undervaluation, M&A is an attractive route for miners to grow production and reserves. Newmont’s USD 17 billion proposal to Newcrest highlights the rising level of interest in M&A among gold majors. It follows the ongoing takeover of Yamana Gold by Agnico-Eagle and Pan American Silver, valued at USD 4.8 billion, announced last year. Newcrest itself completed its acquisition of Pretium Resources during 2022 for USD 2.8 billion. Newmont’s proposal has been rejected, yet Newcrest’s board has indicated it will allow the company access to certain non-public information. We expect further interest from numerous competitors given Newcrest operates some of the sector’s highest quality long-life assets and some exceptional growth assets. The company has demonstrated that it can grow margins, deliver shareholder returns and maintain a healthy balance sheet, making it a compelling target for competitors seeking long-life low-cost growth. Furthermore, given Newcrest’s significant copper exposure there is the potential for major diversified miners to consider a bid. BHP’s recent USD 6.4 billion offer to Oz Minerals, an Australian copper producer, shows that appetite for M&A is building across the mining sector. Interest from major diversified miners would be a significant factor for the final valuation of any Newcrest deal.

Constructive M&A can create value for a company and its shareholders, and M&A is particularly key for the gold industry given the scarcity of precious metals deposits. Low levels of discovery over the past decade have resulted in a shortage of new gold deposits, amid declining grades. Yet M&A activity also brings risk. During the last gold bull market cycle, in 2000’s and early 2010’s, the sector saw examples of value-destructive M&A deals undertaken at sizeable premiums, which resulted in substantial write-offs for the industry in the early 2010’s. Today however, many leading producers appear to have learned the lessons of the last cycle, and the environment for deal-making is constructive. The current wave of M&A deals in the gold sector can be traced back to the historic merger of Barrick Gold and Randgold Resources in 2018. The Barrick/Randgold deal combined Barrick’s portfolio of Tier 1 assets with Randgold’s highly-regarded management, creating a new entity focused on value and delivering returns for shareholders. The transaction took place at no premium, setting an important precedent for M&A in the gold sector and illustrating a sea-change from the value-destructive acquisitions seen during the last cycle.

Since then, the gold sector has seen a series of notable mergers between majors. Newmont Mining acquired Goldcorp in 2019 in a USD 10 billion deal which brought benefits of scale to Newmont’s production. Agnico-Eagle and Kirkland Lake completed their merger of equals in early-2022, creating a senior gold producer. In addition to deal making between the large-cap miners, M&A activity has also been strong among the mid-caps. Great Bear Resources, a Canadian explorer, was acquired by Kinross Gold for USD 1.4 billion during 2022. Recent weeks have seen B2Gold bidding USD 824 million for Sabina Gold & Silver, a Canadian development stage company, highlighting the benefits of a developer selling to a producer with a significantly lower cost of capital, allowing the developer a large value uplift.

Lithium assets in demand – Miners and car manufacturers seek the critical metals to power the EV revolution

Lithium’s central role in the clean energy transition, most notably as a key component of the lithium-ion batteries which power EVs, has put the lithium industry in the spotlight in recent years and sent lithium prices to all-time highs last year amid soaring demand projections, before undergoing a sharp pull-back at the start of 2023. Lithium producers and assets have attracted significant interest as companies seek to expand into this fast-growing sector.

Figure 2

Source: Baker Steel Capital Managers LLP, Albemarle, Bloomberg, S&P, Company Reports. Note, estimated lithium carbonate equivalent (LCE) demand is based on November 2022 data and includes EV, grid, mobility, consumer electronics, industrial and inventory change.

Despite the lithium sector’s lofty recent valuations, major diversified miners are actively seeking deals to capitalise on the strong outlook for the lithium sector. Rio Tinto has acknowledged lithium assets as high priority targets for acquisitions, while also recognising the need to avoid rushing into potentially high-cost deals. Last year the company bought the Rincon Lithium project in Argentina for USD 825m and is keen to grow its lithium business further, particularly after its flagship Jadar lithium project in Serbia had its licenses revoked following large-scale protects against the planned mine. Rio’s value-driven approach to potential deals is typical of the level of discipline in the mining sector today, with most management teams preferring to focus on shareholder returns rather than rush into deals. In contrast, it is notable that Chinese companies have accounted for a large portion of recent deals, given the countries dominance of battery manufacturing. China accounts for around 36% of lithium demand, while around 59% of lithium processing for use in lithium-ion batteries is undertaken in the country.

A further significant development for the lithium industry has been the entrance of original equipment manufacturers (“OEM”), notably car manufacturers into the sector, seeking to secure their battery metals supply chains. While an array of technical challenges will face an OEM entering the mining industry, the benefits of owning stakes in lithium miners, as opposed to relying on supply contracts, is clear. Tesla’s high-profile foray into lithium production began in earnest in 2020 with the acquisition of lithium-rich clay deposits in Nevada, and it is reported that the company is currently considering acquiring Sigma Lithium, which operates a development stage lithium project in Brazil. Similarly, in January 2023 General Motors announced joint investment with Lithium Americas to develop the Thacker Pass mine in Nevada, the largest known source of lithium in the US.

We expect M&A activity in the lithium sector to remain strong, as both miners and OEMs potentially bid for lithium assets. Oil and gas companies may also enter the sector. Bullish projections from the industry indicate a significant supply deficit lies ahead. Albemarle’s forecasts that demand for lithium carbonate equivalent (“LCE”) will rise to 3.7MMt by 2030, compared with 0.8mt in 2022, while mined supply is forecast to reach just 2.9mt by the end of the decade. The key driver behind the transformation of demand and supply dynamics for the lithium sector is government initiatives, most importantly the Inflation Reduction Act, signed into law by the Biden Administration last year, which has encouraged US domestic development of battery supply chains and green infrastructure.

Investors and companies prepare for the next phase of the commodity bull market

Rising M&A activity in the mining sector reinforces our view that the sector is in good health. With so much value among miners right now, we believe many companies could benefit from consolidation, to position themselves for the strong period we believe lies ahead for commodity prices.

With regard to the precious metals sector, gold and silver miners appear significantly undervalued on both a fundamental and relative basis. Margins are strong, yet bull market over-exuberance certainly appears a long way off and capital discipline remains prevalent. Gold equities have pulled back from the highs of 2020, impacted by the dual headwinds of rising US interest rates and US dollar strength. However, with signs the US rate hike cycle is nearing completion, despite inflation remaining elevated, and with the US dollar having seemingly peaked, the outlook for gold and gold equities is improving. We see a range of positive drivers for gold and silver, including rising demand for real assets, persistent inflationary pressure, monetary debasement and rising economic risk.

Within the broader mining sector, we believe the green energy transition will continue to be a major secular growth trend, impacting certain sub-sectors disproportionately as demand surges for the critical materials needed for green technology. The lithium sector is a prime example of this trend and the wave of M&A activity underway illustrates the urgency for miners and OEMs to secure lithium supplies to meet demand for batteries, EVs and broader green industry.

As active managers and long-term investors in the natural resources sector, we are encouraged by the mining sector’s prospects, following years of improvements to balance sheets and margins. The current revival of M&A among majors presents a further source of value for investors in this sector, alongside the operational leverage to higher commodity prices offered by miners. With an increasingly supportive macroeconomic backdrop, strong secular trends for commodity demand, and evidence of constructive M&A underway, we believe a rewarding period lies ahead for mining investors.

About Baker Steel Capital Managers LLP

Baker Steel Capital Managers LLP manages three award winning investment strategies, covering precious metals equities, speciality metals equities and diversified mining.

Baker Steel has a strong track record of outperformance relative to its peers and relative to passive investments in the metals and mining sector. Fund Managers Mark Burridge and David Baker have been awarded two Sauren Gold Medals for 2022 and were awarded Fund Manager of the Year at the 2019 Mines & Money Awards.

Baker Steel’s precious metals equities strategy is a 2023 winner for the sixth year running of the Lipper Fund Awards while Baker Steel Resources Trust has been named Investment Company of the Year 2021, 2020, 2019, Natural Resources, by Investment Week.

Sources: S&P, USGS, Benchmark Mineral Intelligence, Albemarle, Bloomberg, Bloomberg New Energy Finance.

Important

Please Note: This document is a financial promotion is issued by Baker Steel Capital Managers LLP (a limited liability partnership registered in England, No. OC301191 and authorised and regulated by the Financial Conduct Authority) for the information of a limited number of institutional investors (as defined in the Fund prospectus) on a confidential basis solely for the use of the person to whom it has been addressed. This document does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe or purchase any shares or any other interests nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefor. Recipients of this document who intend to apply for shares or interests in Baker Steel’s funds are reminded that any such application may be made solely on the basis of the information and opinions contained in the relevant prospectus or other offering document relating thereto, which may be different from the information and opinions contained in this document. This report may not be reproduced or provided to any other person and any other person should not rely upon the contents. The distribution of this information does not constitute or form part of any offer to participate in any investment. This report does not purport to give investment advice in any way. Past performance should not be relied upon as an indication of future performance. Future performance may be materially worse than past performance and may cause substantial or total loss.