Since emerging as one of the most critical commodities of the decade, lithium has attracted heightened attention from investors, industry and governments. As economies transition from fossil fuels to clean energy sources, the rapid development of electric infrastructure and battery technology requires unprecedented quantities of battery metals. Lithium is a principal component for lithium-ion batteries, the dominant technology for electric vehicles (EVs), placing lithium producers in the spotlight as EV production surges. Recent price weakness for lithium belies the constructive momentum in the sector, which faces a transformation in order to meet historic levels of demand.

Yet the lithium sector faces a range of challenges on the supply side, from permitting for new projects, geographical concentration of processing, to resource nationalism and geopolitical competition. To overcome this, Western governments are undertaking meaningful policy efforts to encourage development of domestic supply chains and attract new entrants into the market. Ultimately, there can be no net zero without a sufficient supply of critical metals and materials, and with lithium among the most sought-after commodities, the sub-sector is in a strong position for growth and profitability. As active investors focused on the metals and mining sector, we identify some key trends for lithium miners in the months and years ahead.

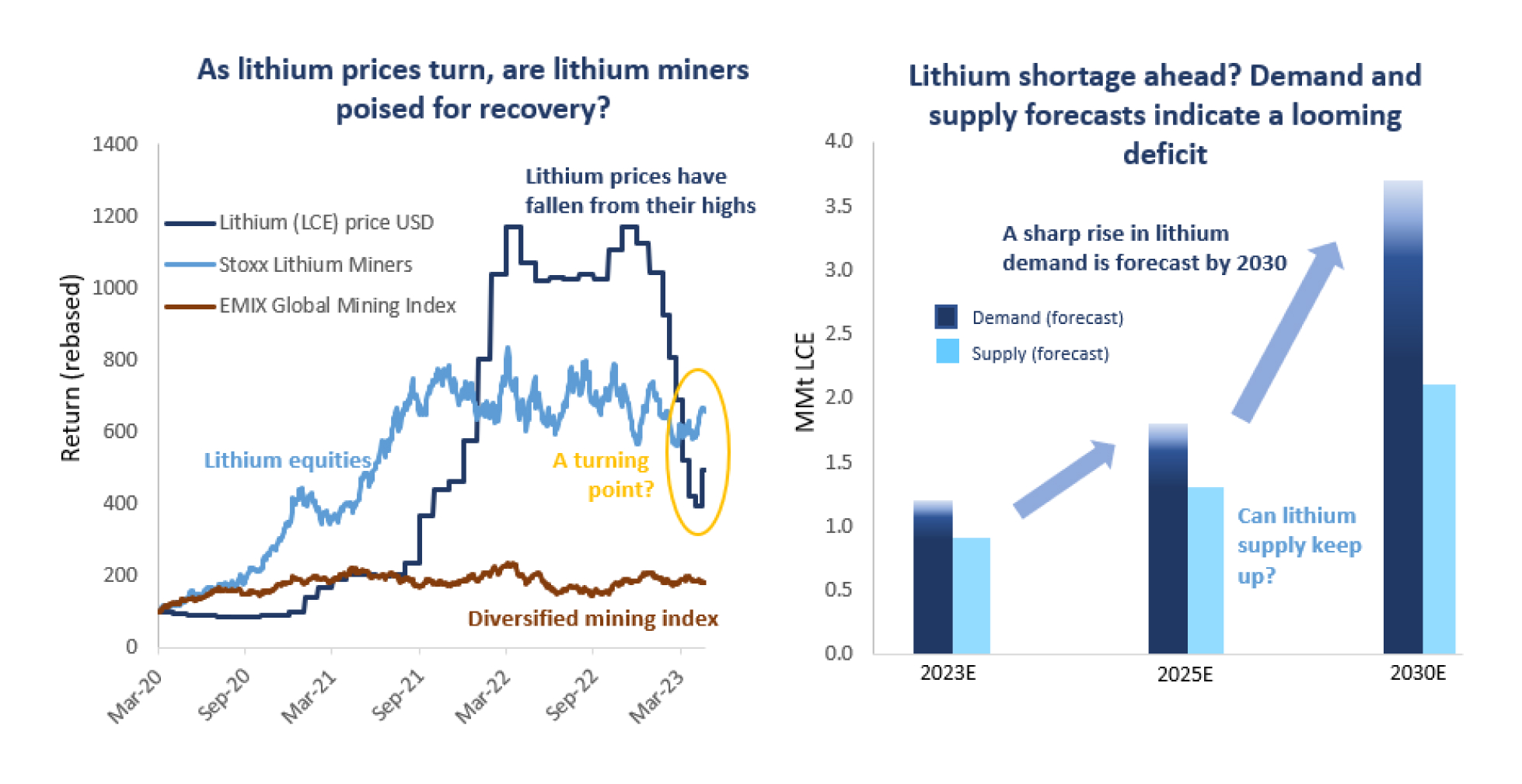

Lithium prices appear to have bottomed following a period of weakness caused by EV market dynamics.

A supply deficit lies ahead as lithium production forecasts fall short of soaring demand forecasts. Political factors, such as potential nationalisation of the lithium industry in Chile, exacerbate the shortfall.

Lithium miners are targets for M&A, as diversified miners, car and battery manufacturers, oil and gas companies, and governments seek to secure their battery metals supply chains.

Volatility may persist as the lithium sector expands, yet miners offer exposure to the growth of the EV and battery industries. Active management is required to identify inflection points in supply and demand.

In few, if any, other sectors is the scale of change due to the green revolution so clear as in the lithium industry. Despite the sector’s rapid recent growth, a shortage of lithium seems all but guaranteed in the years ahead. Supply is expected to rise to around 2.1 million tonnes (mt) by 2030, from 0.9mt in 2023, falling significantly short of the industry demand forecasts which predict demand will jump to 3.7mt by the end of the decade, more than triple the 2023 level.

Figure 1

Source: Bloomberg, Albermarle, Benchmark Mineral Intelligence. Note, demand and supply based on industry forecasts. Data at 22 May 2023.

Lithium faces secular demand growth, backed by rising demand for EVs and batteries

Lithium demand has risen rapidly over the past decade as lithium-ion battery production has ramped up, driven primarily by sharply rising demand for EVs and energy storage. EVs are forecast to account for 18% of global car sales in 2023, having surged from just 3% in 2019. By 2030 EVs are expected to account for 48% of global car sales, representing 46.9m new EVs on the road. Batteries currently account for 80% of global end-use markets for lithium.

Projections for lithium demand have increased each year as the vast scale of industrial requirements becomes clearer. Demand for lithium carbonate equivalent (LCE) is now forecast to rise by around 3x between 2023 and 2030, from 1.2mt this year to 3.7mt by the end of the decade. In particular, the Biden Administration’s recent Inflation Reduction Act has turbo-charged battery supply chain initiatives and electric vehicle plans in North America.

Rapid growth drove lithium prices to an all-time high of around USD 80k/mt LCE in 2022, yet the past year has seen a significant drop in lithium prices, despite the strong outlook for demand in the years ahead. Short-term factors, most notably relating to the Chinese market, were the primary cause of this downward pressure on lithium prices. Rising price competition among car companies in China has resulted in discounting of internal combustion engine vehicles, which has weighed on EV sales. Furthermore, an end to EV subsidies in China has further reduced demand in recent months.

Following this period of consolidation for the sector, we consider that momentum is returning and we see recovery ahead for the lithium price. In the Chinese market, the easing of supply-chain constraints is paving the way for a ramp-up of EV production to meet consumer demand. Meanwhile, Tesla’s recent EV price cut has prompted Volkswagen, BYD, Xpeng, GAC Aion and other rivals to step up subsidies for their own EV models, that will likely stimulate more demand. We expect to see lithium demand rise during the second half of 2023, driven by improving EV sales prospects and thinning lithium stockpiles, amid talk of declining inventories at battery makers. As Chinese battery makers restock, there is a risk of price spikes as some producers will be restocking to fulfil long-term contracts.

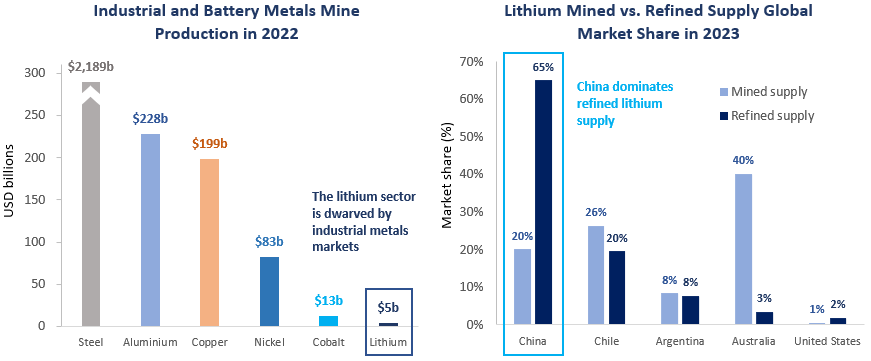

With lithium demand and supply forecasts warning of a significant deficit ahead, increasing production and ensuring security of supply has become a priority for technology companies and manufacturers. The publicly traded lithium sector has grown substantially in recent years, having expanded by an enormous 36x since 2010, with production reaching a value of around USD 4.9 billion in 2022. Despite this rapid growth, the sector remains miniscule compared to major commodity markets and is geographically concentrated, both in terms of mining and processing.

How will politics play a role in lithium supply?

Figure 2

Source: Bloomberg New Energy Finance.

China dominates the supply chain for lithium-ion batteries, particularly on the processing side where it accounts for 65% of refined lithium supply. As US-China tensions continue to rise, the risks for western companies of dependence on Chinese processing of critical raw materials are clear. Chile, another major lithium producer, also presents a risk to supply as the Chilean government considers nationalising its lithium industry. While we believe their approach may ultimately be less extreme, the risk of nationalisation deters miners’ expansion plans in the country, exacerbating the global lithium market’s supply deficit. Geographic and political risk are often considered unavoidable for investors in the mining sector, however we believe risks can be managed through appropriate exposure limits and diversification.

While the lithium industry faces enhanced political risks across key production regions, we consider there are numerous jurisdictions poised for growth, in which we see investment opportunities, including the US, Australia, Canada, Brazil and Argentina. The challenge for the global lithium industry now lies firmly on bringing new mines to production and expanding existing operations as well as accelerating production expansion plans. Permitting for mines and chemical plants in North America and Europe will likely need to be reformed to halve the process time at a minimum, based on industry forecasts. Meeting the expected high levels of demand will require well-capitalised major new entrants into the lithium sector. These producers will need to achieve scale quickly, while a slowdown such as the recent lithium price drop may threaten these companies’ survival.

Government support can play a constructive role in the growth of the lithium industry. In the US, the Department of Energy selected twelve lithium-based projects to be funded with USD 1.6 billion from the 2022 US Bipartisan Infrastructure Law, which aims to support new commercial-scale domestic facilities to extract and process lithium, manufacture battery components, recycle batteries, and develop new technologies to increase US lithium reserves. ESG issues including water usage and community impact are also increasingly important factors for new projects.

Lithium miners in the spotlight

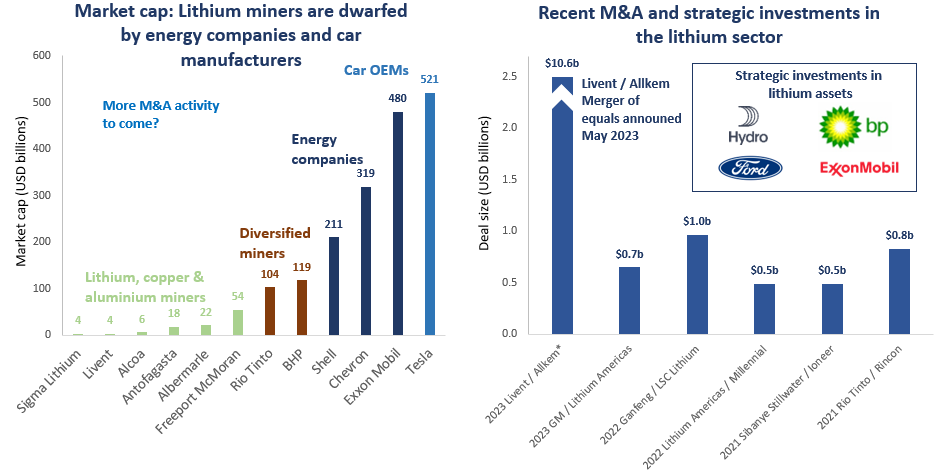

As demand for lithium assets grows, lithium miners are attracting attention from a variety of investors, diversified miners, manufacturers, and technology companies. Many strategic alliances and joint ventures have been established between these companies and lithium producers and explorers, with the objective of ensuring a reliable, diversified supply of lithium for battery suppliers and vehicle manufacturers. A wave of M&A is underway in the lithium sector and expect this to continue, particularly given the small market caps of lithium companies relative to energy companies, manufacturers and diversified miners. Deals can potentially result in significant benefits to shareholders including production ramp-up, cost saving synergies, and valuation uplifts for lithium miners.

Figure 3

Source: Baker Steel Capital Managers LLP, Bloomberg. Data at 28 April 2023.

2023 has seen a marked increase in M&A interest in the lithium sector, prompted in part by recent lithium price weakness. Livent and Allkem’s USD 10.6 billion merger of equals, announced in May, will create the third largest lithium producer globally, in terms of estimated capacity. Two other significant proposed transactions have included Albemarle’s bid to acquire Lionstown, valued at c.USD 5.5 billion and Tesla’s consideration of a potential bid for Sigma Lithium. Both deals were rejected, however the attempts demonstrate the high level of interest in engaging in M&A activity. Furthermore, strategic investments in lithium assets from energy giants BP and ExxonMobil, as well as car manufacturers, notably Ford, and industrial commodity producers, such as Norsk Hydro, highlight the rising flow of capital into the lithium sector. With so much value across the mining sector at present we believe lithium producers, along with many other speciality sub-sectors of the mining industry, can benefit from consolidation, to increase scale and to position themselves for the strong period we believe lies ahead for commodity prices and to ensure lithium supplies can meet demand for batteries, EVs and broader green industry.

We believe the green energy transition will continue to be the most significant secular growth trend for the mining industry in the years ahead, impacting certain sub-sectors disproportionately as demand surges for the critical metals and materials needed for green technology. The lithium sector is a prime example of a beneficiary of this trend, with soaring demand forecasts, supply-side challenges and evidence of rising M&A activity. As active investors in the natural resources sector we seek exposure to high quality lithium mining equities, which are positioned to benefit from the strong tailwinds for the sector, while managing the risks associated with development stage assets, risky jurisdictions and ESG issues such as relative energy intensity and water usage in certain lithium production technologies. It is our view that a passive investment approach in such a rapidly developing sector is not optimal, given the high volatility of many lithium equities and, in the case of the development end of the market, a speculative element. Baker Steel’s actively managed strategy focuses on value as well as growth in our stock selection for lithium equities, while actively adjusting our weighting to this sub-sector relative to others within the mining sector.

As momentum builds for green industries and battery technology development, we believe the new bull market for speciality metals, including lithium, is only just beginning. The mining sector has a central role to play in achieving governments and companies’ net zero objectives, and the years ahead will see these markets transformed by growth and value creation.

About Baker Steel Capital Managers LLP

About Baker Steel Capital Managers LLP

Baker Steel Capital Managers LLP manages three award winning investment strategies, covering precious metals equities, speciality metals equities and diversified mining.

Baker Steel has a strong track record of outperformance relative to its peers and relative to passive investments in the metals and mining sector. BAKERSTEEL Precious Metals Fund is the 2025 winner of the GELD-Magazin Alternative Investment Award, and 2025 winner for the seventh year running of the Lipper Fund Awards while BAKERSTEEL Electrum Fund is the 2025 winner of the Euro Fund Awards Commodity Equities Performance over 10 years. The Baker Steel Resources Trust has also been named Investment Company of the Year 2021, 2020, 2019, Natural Resources, by Investment Week.

Fund Managers Mark Burridge and David Baker have been awarded two Sauren Gold Medals for 2021 and were awarded Fund Manager of the Year at the 2019 Mines & Money Awards.

Important

Please Note: This document is a financial promotion is issued by Baker Steel Capital Managers LLP (a limited liability partnership registered in England, No. OC301191 and authorised and regulated by the Financial Conduct Authority) for the information of a limited number of institutional investors (as defined in the Fund prospectus) on a confidential basis solely for the use of the person to whom it has been addressed. This document does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe or purchase any shares or any other interests nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefor. Recipients of this document who intend to apply for shares or interests in Baker Steel’s funds are reminded that any such application may be made solely on the basis of the information and opinions contained in the relevant prospectus or other offering document relating thereto, which may be different from the information and opinions contained in this document. This report may not be reproduced or provided to any other person and any other person should not rely upon the contents. The distribution of this information does not constitute or form part of any offer to participate in any investment. This report does not purport to give investment advice in any way. Past performance should not be relied upon as an indication of future performance. Future performance may be materially worse than past performance and may cause substantial or total loss.