Gold at a turning point – Will precious metals miners deliver outsized returns in 2024?

The end of the US rate hike cycle, rising economic risk, and strong physical demand may push the gold price to new highs, marking the start of a turnaround for miners.

Gold has largely fulfilled its traditional role in recent years, protecting purchasing power in the face of rampant inflation, and withstanding the headwinds of rising real interest rates and surging US dollar strength. In contrast, precious metals miners, which typically offer operationally leveraged exposure to gold and silver, have faced weakness since late-2020, as mixed investor sentiment towards equities in general, weighed on share prices. Following this period of consolidation, the gold sector now finds itself well-supported by near- and long-term tactical themes, while miners appear historically undervalued despite being in healthy financial shape and paying encouraging dividends.

The catalysts for gold’s move to new highs and precious metals miners’ recovery are increasingly clear. A major macroeconomic shift appears to be underway as the US rate hike cycle turns, inflation fades, and economic risks rise. Historical precedent indicates a strong period ahead for precious metals and, perhaps more so than in previous cycles, we believe that an actively managed precious metals equities strategy can deliver superior returns potential relative to physical gold and silver.

A new bull market for precious metals?

The end of US rate hike cycles historically pushed gold to new highs – In the past three cycles, gold rose >50% in the aftermath of a “pause” in hikes. Conviction is building that the US Fed has finished.

Gold tends to perform well amid economic and geopolitical uncertainty – Economic risk is rising in the US under the “higher for longer” interest rate scenario. Confrontational geopolitics will likely continue.

De-dollarisation is gaining traction – The US share of global trade is retreating, US debt growth is accelerating, and many emerging market central banks are reducing US treasury holdings.

Physical gold demand is robust – Gold jewellery consumption continues to recover from COVID lows amid higher local prices (e.g. yuan, rupee), while central bank buying may reach another record high in 2023.

Gold miners are in strong shape – Miners offer healthy margins and balance sheets, growth, ESG performance and dividends, while constructive M&A continues. The sector remains historically and relatively undervalued.

When will the precious metals sector break out?

Figure 1

Source: Bloomberg, Canaccord Genuity. Data at 31 October 2023.

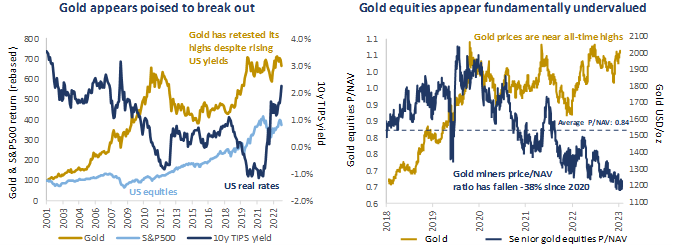

Since hitting its all-time high at the height of the COVID pandemic in the summer of 2020, gold has defied a range of negative market forces and traded between USD 1800-2000/oz for most of the past three years, while re-testing its high three times. This robust performance has been achieved despite the sharpest US interest rate hiking cycle in a generation and with the US dollar hitting a two-decade high. Importantly, gold has continued to make new highs in many other major currencies, including the Euro, Sterling, and Australian and Canadian dollar, during this period.

In contrast, gold mining equities have seen their share prices flounder. On a price-to-NAV (P/NAV) basis gold miners’ valuations have declined -38% over the past three years despite the gold price remaining virtually unchanged. Just to return to their 2020 highs, gold equities would have to rise +69% in nominal terms, and +100% in real terms (MSCI ACWI Select Gold Miners Index, at 31 October 2023). This de-rating has occurred despite the miners themselves benefitting from strong margins, effective operational performance, and robust balance sheets. The question for investors in this long-overlooked sector is: What are the catalysts to push gold to new highs and spark a rally in gold miners?

In the sections ahead, we explore the key drivers which we anticipate will initiate a recovery for the sector in the months ahead and underpin the new bull market for gold, silver and precious metals miners.

Interest rates, inflation and rising economic risk – Has the inflection point been reached?

The most significant potential catalyst for higher gold prices in the months ahead is the end of the US interest rate hiking cycle. Hawkish rhetoric and expectations have proven a headwind for gold, which pays no income, as rising yields sapped demand. Yet with hawkish monetary policy now seemingly priced in and with the US Fed having “paused” rate hikes, we believe an inflection point has been reached whereby the outlook is increasingly favourable for gold.

As illustrated below, the gold price gained over 50% following a “pause” by the US Fed at the end of each of the past three rate hike cycles, in 2000, 2006 and 2019. If this historical precedent holds true, then we should ultimately expect to see gold prices approaching USD 3000/oz as the coming up-cycle gains pace. While as equity-focused investors we do not set target prices or make predictions for physical gold, we believe that this historical trend coupled with recent encouraging gold price performance strongly supports the case that a new bull market for gold and miners lies ahead.

Figure 2

Source: Bloomberg, Baker Steel Capital Managers LLP. Data at 31 October 2023.

Alongside the benefits of steady or falling nominal and real interest rates for the gold sector, we consider that the rising economic risk for the US and globally, amid higher borrowing costs and lacklustre growth, is supportive for higher gold prices. While policymakers stick to the “soft landing” narrative, history shows that economic and financial conditions can change quickly. The full impact of the 5.25% of hikes enacted by the US Fed since early 2022 has likely not yet fed through to the real economy, and as a result we consider the probability of further difficulties for the US economy is substantial. The collapse of Silicon Valley Bank and two other mid-sized lenders in early 2023, which threatened contagion across the financial system, highlighted how swiftly crises can develop. Notably gold and gold equities reacted positively to the banking crisis, with gold re-testing its all-time high and gold miners rallying 17% during March 2023 alone (MSCI ACWI Select Gold Miners Index, in USD terms).

Gold has tended to perform well during periods of economic crisis and geopolitical turmoil, fulfilling its role as a safe haven investment. Economic risks aside, undoubtedly the world remains in a situation of significantly heightened geopolitical tensions, with Russia’s war in Ukraine nearing the end of its second year, Israel’s conflict with Hamas in Gaza threatening to escalate into a regional crisis in the Middle East, and continued tension between the US and China across a range of flashpoints such as trade, supply chains, and Taiwan.

What would de-dollarisation mean for gold?

A key headwind for the gold price has been the surge in US dollar strength over the past three years to a twenty year high. A strong dollar is typically a negative factor for gold and silver which are priced primarily in US dollar terms, as is the case for most commodity markets. Recent rises in the US dollar can largely be attributed to the relative strength of the US economy compared to much of the rest of the world, amid the tumultuous global events of the past few years which saw economies impacted by the COVID pandemic, war in Europe, the fight against climate change, as well as the return of inflation. There are however signs this dynamic may be starting to shift.

Figure 3

Source: Bloomberg, Baker Steel Capital Managers LLP. Data at 31 October 2023.

While the USA’s status as the world’s pre-eminent economic power and the US dollar’s reserve currency status are not under threat, certain trends suggest the US’s dominance may be becoming more precarious. The deterioration of US public finances is well-publicised, with US debt totalling over USD 33 trillion, a USD 1.7 trillion deficit, and over USD 1 trillion cost of debt servicing for 2023. To put this in context, total US Government tax revenue was around USD 5 trillion in 2022, meaning that c.20% of the US tax take was spent on debt interest. This highlights starkly the scale of the risk to the US budget posed by the sharp rises in public debt in recent years and the impact of higher interest rates.

Figure 4

Source: Bloomberg, World Gold Council. Data at 31 October 2023.

Furthermore, the erosion of the US’s share of global trade, amid geopolitical and strategic realignments, points towards potential de-dollarisation, notably in emerging markets. Not only are rising US rates and a strong dollar a problematic factor for emerging market countries with dollar-denominated debt, but the Russia-Ukraine war brought into sharp focus the risks of holding US debt. Notably China has been reducing its US Treasury holdings, as have certain other BRICS economies. Trade is another area in which the influence of the US dollar is receding, most notably in the oil market where sales are increasingly being paid for in non-US dollar currencies.

While de-dollarisation is at an early stage and is unlikely to rapidly occur, the longer-term implications are significant, re-shaping the global economy and adjusting the balance of power between countries and blocs. The resulting reduction in demand for dollars would indicate a weakening of the currency over time. As countries seek alternatives to the US dollar, we believe gold has a role to play as a stable financial asset and proven safe haven investment, with a low correlation to broader financial markets. The relevance of gold for policymakers is exemplified by central banks’ purchasing of physical gold, which hit an all-time high in 2022 and appears similarly strong in 2023.

Unearthing returns in precious metals miners – Active investment management offers superior upside potential

As long-term investors in the precious metals equities sector, recent market conditions have proven challenging and at times frustrating. We consider our key objective as active investment managers in this environment has been to successfully maintain our precious metals equities strategy’s fundamental upside potential, while minimising risk without going defensive. Having largely achieved this, we now find ourselves in a situation where precious metals mining equities appear amongst the most undervalued sectors across all equity markets, amid signs a turning point is near. The key catalyst for gold equities to recover is a sustained rise in the gold price, boosting producers’ profitability and sparking a recovery of investor sentiment and interest in this frequently overlooked sector. In previous up-cycles, gold equities have tended to deliver 2-5x leverage to the rising gold price, delivering potentially astounding returns over a short period of time.

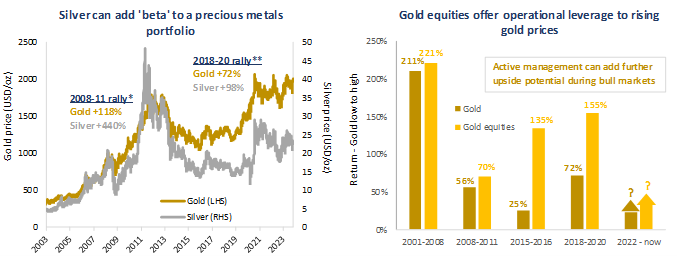

Value-driven stock selection is key to Baker Steel’s investment process, but our team also add value through tactical asset allocation driven by our views on supply and demand dynamics, sub-sector valuations and macroeconomic outlook. For this reason, Baker Steel currently has a high weighting to silver miners both in our precious metals equity strategy and also in our speciality metals mining strategy, “Electrum”. As both a precious and industrial metal, we regard silver to have strong recovery potential under a rising gold price environment as well as having supportive supply and demand dynamics, as demand for silver for solar photovoltaic cell production is forecast to rise. Silver has tended to outperform gold during previous bull markets (see chart below) and we are confident that an allocation to silver miners offers outsized returns potential as the sector’s recovery gains pace.

Figure 5

Source: Bloomberg, Baker Steel internal. Data 31 October 2023. *Data from 30/09/2008 to 05/09/2011. **03/10/2018 to 06/08/2020. Note, Gold Equities represented by XAU Index.

Today we believe the outlook for the precious metals sector is more positive than it has been for many years; likely since the end of the last US rate hike cycle in early 2019. But beyond the supportive macroeconomic themes, we consider that the current state of the precious metals sector offers opportunities for active management to add value. The wave of constructive M&A underway in the gold sector at present exemplifies this, given that it is driven by two key factors. Firstly, emerging companies which struggle to raise finance must increasingly turn to larger producers. With the balance of opportunity now on the side of the mid-sized and larger companies, favourable opportunities exist for the mid-to large-cap portion of the sector in which Baker Steel tends to invest. Secondly, the recent merger of Newmont Mining and Newcrest Mining, two major gold producers, will result in a string of non-core (but still quality) asset divestments, offering opportunities for acquisition by mid-cap companies for whom these assets are highly significant. We believe active stock selection will be key to unlocking M&A opportunities relative to a passive investment in the sector.

As a team with multi-cycle investment experience, we know that investment success in this sector is typically the result of a combination of factors. Our value-driven investment philosophy, proprietary research tools and active investment approach have been central. Yet, it is the technical prowess of our team which we believe to be the biggest driver of investment success. As an independently owned firm our Managing Partners, as Fund Managers, are closely aligned with our investors, and with the Baker Steel Investment Team having expanded this year, we have ensured our research capacity is growing with the strategy and with the sector’s progress.

As we approach what we believe will be a highly supportive environment for gold and precious metals miners in 2024 and beyond, Baker Steel’s team continues to deliver our unique and value driven investment approach, to the benefit of our clients, while adhering to sector leading ESG practices.

About Baker Steel Capital Managers LLP

About Baker Steel Capital Managers LLP

Baker Steel Capital Managers LLP manages three award winning investment strategies, covering precious metals equities, speciality metals equities and diversified mining.

Baker Steel has a strong track record of outperformance relative to its peers and relative to passive investments in the metals and mining sector. BAKERSTEEL Precious Metals Fund is the 2025 winner of the GELD-Magazin Alternative Investment Award, and 2025 winner for the seventh year running of the Lipper Fund Awards while BAKERSTEEL Electrum Fund is the 2025 winner of the Euro Fund Awards Commodity Equities Performance over 10 years. The Baker Steel Resources Trust has also been named Investment Company of the Year 2021, 2020, 2019, Natural Resources, by Investment Week.

Fund Managers Mark Burridge and David Baker have been awarded two Sauren Gold Medals for 2021 and were awarded Fund Manager of the Year at the 2019 Mines & Money Awards.

Important

Please Note: This document is a financial promotion is issued by Baker Steel Capital Managers LLP (a limited liability partnership registered in England, No. OC301191 and authorised and regulated by the Financial Conduct Authority) for the information of a limited number of institutional investors (as defined in the Fund prospectus) on a confidential basis solely for the use of the person to whom it has been addressed. This document does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe or purchase any shares or any other interests nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefor. Recipients of this document who intend to apply for shares or interests in Baker Steel’s funds are reminded that any such application may be made solely on the basis of the information and opinions contained in the relevant prospectus or other offering document relating thereto, which may be different from the information and opinions contained in this document. This report may not be reproduced or provided to any other person and any other person should not rely upon the contents. The distribution of this information does not constitute or form part of any offer to participate in any investment. This report does not purport to give investment advice in any way. Past performance should not be relied upon as an indication of future performance. Future performance may be materially worse than past performance and may cause substantial or total loss.