The gold sector faces conflicting macroeconomic and market forces at present, as bullish demand drivers such as surging inflation, rising economic risk and geopolitical tension, are counter-balanced by headwinds for gold, most notably the steepest US rate hikes and strongest US dollar in two-decades.

Amid these challenging market conditions gold has declined by around 5% in US dollar terms since the start of 2022, yet despite this the metal appears resilient relative to global equity markets which have suffered far heavier losses as investors adapt to tighter monetary conditions. Gold miners have fared worse than physical gold, suffering a more significant sell-off in recent months, despite many producers benefitting from strong margins, disciplined cost control, and continuing to pay dividends.

Market conditions are evolving rapidly and, with risks to economic growth rising, we see a change in fortunes ahead for the beleaguered gold sector. Higher borrowing costs, supply chain shocks and declining consumer spending, indicate slower growth ahead for economies already battered by the highest inflation since the 1970s and the residual impact of the COVID-19 pandemic. As the US rate hike cycle runs its course and policymakers’ attention shifts towards supporting slowing economies, we anticipate a return of momentum for gold and gold equities.

Is gold at a turning point?

Real assets such as gold are positioned to outperform – Gold is the ultimate real asset and offers a hedge against persistent inflation as well as portfolio protection against the risk of economic slowdown. Historically, gold and gold equities tend to outperform general equity markets during periods of recession and stagflation, as well as performing well during periods of inflationary growth.

Hawkish rate targets appear priced in and the catalysts for gold’s recovery are clear – Any undershoot of the Fed’s rate hike targets would likely spark a rally for precious metals. Meanwhile supply-side inflation is expected to persist, indicating a strong case for the recovery of precious metals during the second half of 2022.

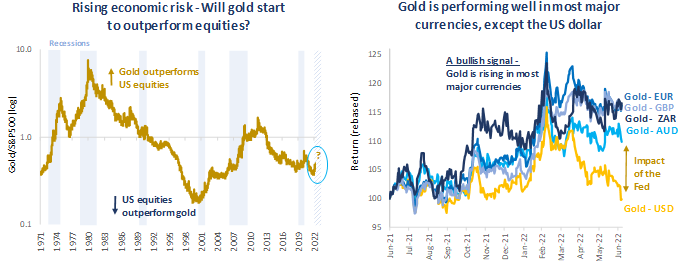

Figure 1

Source: Baker Steel internal, Bloomberg. Data at 18 July 2022. Note, Gold in Major Currencies includes EUR, GBP, AUD and ZAR.

Inflation is here – Why hasn’t gold performed?

Inflation has hit multi-decade highs in the US and Europe, driven by a multitude of factors from rebounding consumer demand post-COVID, to supply-side challenges due to choked-up supply chains and extreme tightness in labour markets. The Russia-Ukraine conflict has compounded these challenges, causing food and energy prices to soar.

Inflation has historically been supportive for gold and silver prices, alongside broader commodities, however hawkish rhetoric from the Fed has instead sapped investor sentiment towards the sector, as policymakers stick resolutely to their core objective to reduce inflation, notwithstanding the serious risks posed by higher rates to economic growth and business activity. Rising real interest rates tend to be negative for gold, and with the attention of investors and market commentators in recent months remaining firmly fixated on the speed and scope of US interest rate hikes, the gold price has so far been constrained from appreciation in response to inflation.

Yet as the interest rate hike cycle progresses, we are approaching an inflection point at which the scope for further rate hikes becomes less feasible, due to the severe impact on indebted businesses and consumers, and policymakers’ focus will likely shift towards protecting employment. We believe the hawkish rate hike programme is now largely priced into the gold sector, hence any shift in policy toward a more accommodative stance should prove a catalyst for the next bull market phase for gold, particularly as inflation, which we believe to be predominantly supply-side driven, is unlikely to be fully tamed by rate hikes.

How do gold and gold equities perform during recession and stagflation?

The global economic outlook remains clouded, with a range of major banks now attributing a worryingly high probability to economic slowdown. Our team’s core view remains that the policymakers will shift their focus towards growth in the coming months, accepting that inflation will run higher for longer, particularly as the impact of higher rates on the real economy becomes apparent. However, we also recognise that stagflation is now also a distinct possibility, as inflation persists and growth stagnates.

The gold sector has proven itself a worthwhile investment during times of economic hardship, most recently during the COVID-19 pandemic, and before that during the European debt crises of the 2010s and during the Global Financial Crisis. However, to see how gold and gold equities have historically performed under an environment of stagflation, we must look back to the 1970’s, as illustrated on the charts below.

How did gold and gold equities perform during the 1970s?

The similarities with the economic conditions of the 1970s are notable. Inflation in the early-70s was being driven by rising energy costs, including the 1973 energy crisis, as well as labour issues caused by trade unionist activity, against a backdrop of rapid deficit expansion to fund the Vietnam war. One major driver, which echoes today’s economic environment, is mismanagement by central bankers and policymakers, as price rises were stoked by inflationary monetary and fiscal policies. Today we see strong similarities, as central bankers adopt overtly hawkish stances with the hope of compensating for years of ultra-loose monetary policy and money printing. The inflation of the late-1970s highlighted the persistence of these inflationary forces, which were further compounded by tense geopolitical events, such as the Iranian Revolution and the Soviet invasion of Afghanistan. During both periods of inflation, gold and gold equities delivered strong outperformance of broader equity markets, as investors sought exposure to real assets and protection from economic risks. Today, should the risk of stagflation continue to grow, we believe precious metals and miners are positioned to outperform broader financial markets once again. The recent sell-off may present a worthwhile point for investors to build exposure to the precious metals sector, which has historically shown that it can be a safe haven from rising financial sector risk, recession risk and inflationary pressure. As always, the high level of uncertainty across markets makes it virtually impossible to “pick the bottom”.

Looking ahead, after a decade or more out of favour among many generalist investors, gold appears positioned to enjoy a period of outperformance relative to broader financial markets. We see a further opportunity in gold miners, which remain undervalued on both a fundamental and relative level and are in healthy financial shape. To give some perspective, the last time the gold price was at c.USD 1725/oz in mid-2021, miners’ share prices were around 30% higher than today. Strikingly, in order just to regain their 2020 highs gold miners would need to rebound by around 75% (EMIX Global Mining Gold Index, in US dollar terms).

Upcoming results from the gold sector are expected to show that a selection of high-quality miners are maintaining strong margins and demonstrating operational success, while others face rising costs and operational challenges. In our view this underscores the need for active management in the precious metals equities sector. We remain focused on those producers who are best placed to control costs, protect margins and raise their dividends, with the goal of delivering superior risk adjusted returns, relative to a passive holding in physical gold or gold equities.

About Baker Steel Capital Managers LLP

Baker Steel Capital Managers LLP manages three award winning investment strategies, covering precious metals equities, speciality metals equities and diversified mining.

Baker Steel has a strong track record of outperformance relative to its peers and relative to passive investments in the metals and mining sector. Fund Managers Mark Burridge and David Baker have been awarded two Sauren Gold Medals for 2022 and were awarded Fund Manager of the Year at the 2019 Mines & Money Awards.

Baker Steel’s precious metals equities strategy is a 2023 winner for the sixth year running of the Lipper Fund Awards while Baker Steel Resources Trust has been named Investment Company of the Year 2021, 2020, 2019, Natural Resources, by Investment Week.

Sources: S&P, USGS, Benchmark Mineral Intelligence, Albemarle, Bloomberg, Bloomberg New Energy Finance.

Important

Please Note: This document is a financial promotion is issued by Baker Steel Capital Managers LLP (a limited liability partnership registered in England, No. OC301191 and authorised and regulated by the Financial Conduct Authority) for the information of a limited number of institutional investors (as defined in the Fund prospectus) on a confidential basis solely for the use of the person to whom it has been addressed. This document does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe or purchase any shares or any other interests nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefor. Recipients of this document who intend to apply for shares or interests in Baker Steel’s funds are reminded that any such application may be made solely on the basis of the information and opinions contained in the relevant prospectus or other offering document relating thereto, which may be different from the information and opinions contained in this document. This report may not be reproduced or provided to any other person and any other person should not rely upon the contents. The distribution of this information does not constitute or form part of any offer to participate in any investment. This report does not purport to give investment advice in any way. Past performance should not be relied upon as an indication of future performance. Future performance may be materially worse than past performance and may cause substantial or total loss.