Rare Earths – A scramble for supplies, an opportunity for investors

Vital for green technology, rare earths are not geologically ‘rare’ yet face precarious supply chains with a scarcity of production and processing in the West.

The 17 elements known as rare earths are critical for a wide range of technologies across industries globally, yet China dominates the rare earth supply chain, from active deposits to processing. Rare earth metals present a valuable example of the investment themes which we target through Baker Steel’s Electrum strategy, focusing on the “future facing” metals and materials which face surging demand from the green revolution. Given the recent fall in rare earth prices and related equities set against the robust longer-term outlook, we believe rare earths’ precarious supply dynamics present both risks and opportunities for investors:

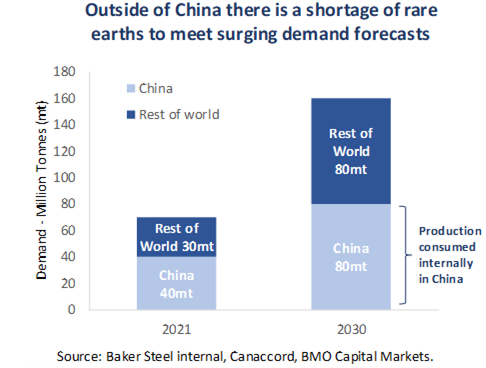

Demand for magnet rare earths is forecast to more than double by 2030, driven by the green revolution. Outside of China there is already a real issue in securing enough material and processing to magnet stage.

Rising geopolitical tension, particularly between the US and China, will likely place further strain on supply chains for rare earths. Securing the supply of critical materials, while protecting sensitive technologies, is increasingly difficult for governments and holds significant implications for naturals resources investors.

As active investors and commodity-equity specialists, we are invested in selected Western producers and processors of rare earths, which we believe will trade at higher multiples as the market comes to appreciate the challenges involved in permitting, producing and processing rare earths.

Demand for rare earths is soaring – Why are these elements so important?

Rare earths are in fact relatively common elements, with the ‘rare’ label referring to the low grades in which they are found, rather than geological scarcity. They are generally defined according to weight, with 8 light (atomic number below 62) and 9 heavy rare earths (>62). The primary use of rare earths is in the hi-tech sector, notably in magnets and in electronics. Permanent magnets, which are used in EVs and wind turbines, are a particularly strong area of demand growth. Four rare earth elements are needed to make magnets, the two primary ‘light elements’ are Neodymium (Nd) and Praseodymium (Pr). The two ‘heavy’ sweeteners, which enhance magnet performance, are Dysprosium (Dy) and Terbium (Tb). The price of NdPr had risen by around 300% over the past two years until the recent pullback. These now appear well-supported, given their critical usage across many technologies.

We expect demand to more than double by the end of the decade for the magnet rare earths. Value-in-use estimates for NdPr in EVs and wind turbines are orders of magnitude above current levels. A rule of thumb for EV production is that NdPr magnets can reduce battery pack sizes by up to a third, so around USD 2k per car. For wind turbines the costs are under 0.5% of the total. These bullish numbers do however hide significant substitution risk from improvements in alternative magnet designs which have already enabled some reduction in EV related rare earth magnet demand.

Figure 1

Source: Baker Steel internal, Canaccord, BMO Capital Markets

With fragile supply chains, can industry get the rare earths it needs?

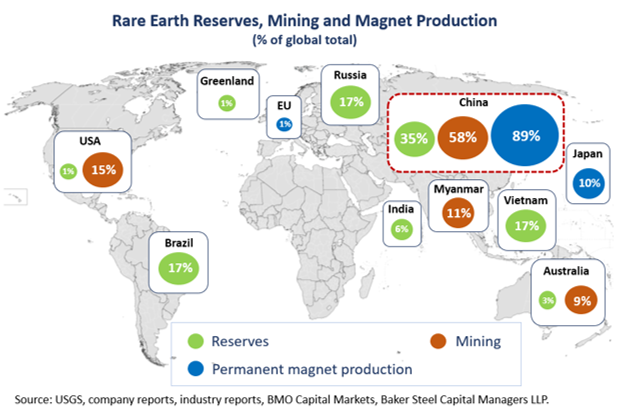

While geologically abundant, the supply of rare earths for industrial use is currently geographically concentrated in one country, China, which accounts for around 35% of global reserves, 58% of mine production and 87% of separation. Ultimately around 8% of rare earth metals alloys and around 89% of magnet rare earths come from China. China continues to have the world’s best rare earth deposits and, despite declining grades and rising costs, has leveraged this advantage to become the dominant country throughout the supply chain. Yet, Chinese mine production appears unlikely to grow at the required rate to meet global demand so there is now a real need for development of rare earth production and processing outside of China.

Figure 2

Source: USGS, company reports, industry reports, BMO Capital Mrkets, Baker Steel Capital Managers LLP

Historically the rare earth market has not always been so concentrated. From 1945 to 2000 the US and Russia dominated the sector, before China’s entry to the market in the 1990s and production ramp-up in the 2000s caused rare earth prices to collapse, sending non-Chinese mines out of business. Today China has two main production centres, one for light rare earths and a second with a larger proportion of heavy rare earths, split by the north and southern regions respectively. China’s downstream value chain, from separation stage onwards, has been developed since about 2005.

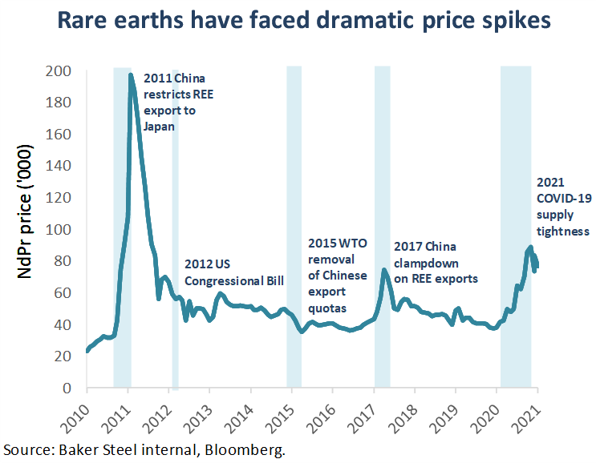

2010 saw rare earths become ‘weaponised’ by China for the first time, during its trade dispute with Japan. The resulting price spikes saw the ‘heavy’ rare earths Dysprosium (Dy) and Terbium (Tb) rise by around 5,000%. Following this volatility, non-Chinese sources of rare earths became ‘strategic’ assets, fuelling an exploration boom involving hundreds of junior mining companies. Despite western governments pledging to support domestic mining and processing of rare earths, just two mines were built. The Mount Weld mine in Western Australia is operated by Lynas Rare Earths, and has processing in Malaysia, while the Mountain Pass mine is located in the USA, with domestic processing and is operated by Molycorp. Rare earth prices collapsed shortly after both mines went into production, as export quotas were lifted and demand stabilised for what are now considered the “low-value” rare earths. Molycorp went bust during this period, while Lynas barely survived, operating at a substantially smaller scale than planned.

Figure 3

Source: Baker Steel internal, Bloomberg

Since 2011 US administrations have repeatedly tried to regain some of their share of the rare earth sector, in order to protect against Chinese-driven price volatility and supply chain issues. The 2011-2012 congressional bill aimed to encourage investment, exploration, and development of domestic rare earths, and to boost long-term secure supply for the US. These efforts proved largely unsuccessful and Chinese dominance has continued to increase over the subsequent decade. Price volatility, driven by Chinese policy towards the rare earths sector, has also continued (as highlighted by the chart above). The 2015 WTO ruling forcing China to abandon export restrictions sent rare earth prices into a slump, before China’s clampdown on exports of rare earths in 2017 caused a renewed spike in prices. In recent years, supply chain tightness, compounded by COVID-19 restrictions in China has sent rare earth prices back to 10-year highs. Recent years have also seen a sharp rise in concerns among policymakers and industry leaders regarding the fragile supply chains which underlie the rare earth sector which we should expect given these materials’ application in green transition technologies and defence technology. Increasingly open economic and geopolitical competition between the US and China has added further tension to the issue. Under the Biden administration efforts have continued to increase and strengthen US supplies, with the 2022 “REEShore Act”, aimed at increasing the production and storage of rare earths in the US, while restricting the use of Chinese-made rare earth products in military technologies. However, we view the recently announced Inflation Reduction Act as by far the most significant government intervention to date, and we aim to produce a separate analysis of this shortly for publication.

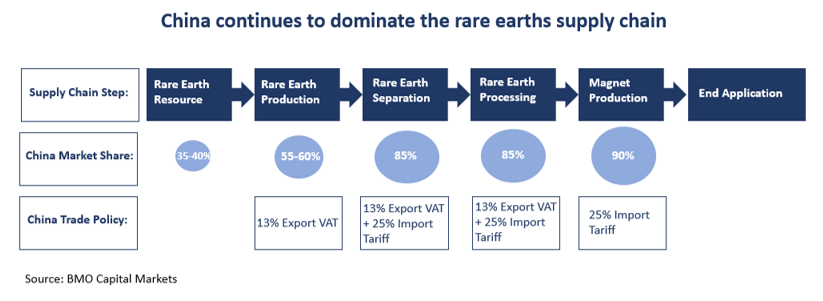

Figure 4

Source: BMO Capital Markets

While growing recognition of the risks of the West’s reliance on Chinese rare earth supply is driving efforts by policymakers and industry leaders to seek alternative sources of supply, the challenge is substantial. Today, non-Chinese rare earth mining accounts for c.40% of the market but c.75% of that goes into China for further processing, while no semi-finished Chinese products are exported. Non-Chinese magnet demand today, required for windfarms and EVs, is estimated at c.35% of the global total, or 30ktpa of NdPr. Yet only 7ktpa of NdPr magnets can be produced outside of China, leaving western industries reliant on China to export 23ktpa. The 25% increase in Chinese export quotas in August has again depressed rare earth prices to a point where many projects would not be feasible.

Not only does China’s focus on magnet production involve adding value at each step in the supply chain, but it also implements tariffs at each stage, effectively protecting the Chinese domestic market. Looking ahead, we project that Chinese end-use demand will rise to around 80ktpa by 2030, from c.40kpta today (NdPr equivalent numbers). In simple terms, this means that all else being equal, all Chinese magnets that currently supply the rest of the world, will no longer be exported.

Assuming a similar growth rate for non-Chinese industries, magnet production will need to increase from 7ktpa to 60ktpa, equating to over 300Ktpa of rare earth oxide production. The reality is more nuanced as the heavy rare earth sweeteners DyTb needed in those magnets are only found in certain types of deposit, most notably ionic clays. Given this expected increase in production, 4ktpa of DyTb will be needed outside of China (assuming a 15:1 ratio) by 2030. With an average grade of 2% from the ionic clays, this implies 200ktpa of rare earth oxide, just for DyTb (albeit with some by-product of the light rare earths, NdPr). While modern techniques allow processors to separate one rare earth from the other relatively inexpensively, with improved separation techniques being developed, it remains practically impossible to simply mine and refine one, or two, rare earths at a time.

Investing in producers and processors of rare earths – The vital elements for the green revolution

Given the vital role played by rare earths across a range of strategically important technologies, we consider the years ahead to hold promise for investors in this sector. Appreciation of the risks of China-dominated supply chains is growing, as is the political will to encourage development of Western production and processing of rare earths.

Through our Electrum strategy, we are currently invested in one of only two non-Chinese owned producers, which covers downstream rare earth products, from rare earth oxide to magnets. We believe the processing and permitting challenges of rare earth oxide, alloy and magnet production are vastly underestimated by the market and consider that as these difficulties become better appreciated the market will pay a higher multiple. In the meantime, we enjoy a dividend as the company generates a very healthy free cash yield and growth at a much lower capex intensity than peers.

With long-term prices appearing well-supported, for the magnet rare earth metals at least, the investment case for rare earth producers is compelling. Outside of China there is a real challenge for companies to secure enough material, and to be able to process that to the magnet stage. As active investors and commodity-equity specialists, we consider rare earth producers to be a prime example of a “future facing” sub-sector of the natural resources sector, offering value and growth as demand for secure and sustainable supply grows.

About Baker Steel Capital Managers LLP

About Baker Steel Capital Managers LLP

Baker Steel Capital Managers LLP manages three award winning investment strategies, covering precious metals equities, speciality metals equities and diversified mining.

Baker Steel has a strong track record of outperformance relative to its peers and relative to passive investments in the metals and mining sector. BAKERSTEEL Precious Metals Fund is the 2025 winner of the GELD-Magazin Alternative Investment Award, and 2025 winner for the seventh year running of the Lipper Fund Awards while BAKERSTEEL Electrum Fund is the 2025 winner of the Euro Fund Awards Commodity Equities Performance over 10 years. The Baker Steel Resources Trust has also been named Investment Company of the Year 2021, 2020, 2019, Natural Resources, by Investment Week.

Fund Managers Mark Burridge and David Baker have been awarded two Sauren Gold Medals for 2021 and were awarded Fund Manager of the Year at the 2019 Mines & Money Awards.

Important

Please Note: This document is a financial promotion is issued by Baker Steel Capital Managers LLP (a limited liability partnership registered in England, No. OC301191 and authorised and regulated by the Financial Conduct Authority) for the information of a limited number of institutional investors (as defined in the Fund prospectus) on a confidential basis solely for the use of the person to whom it has been addressed. This document does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe or purchase any shares or any other interests nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefor. Recipients of this document who intend to apply for shares or interests in Baker Steel’s funds are reminded that any such application may be made solely on the basis of the information and opinions contained in the relevant prospectus or other offering document relating thereto, which may be different from the information and opinions contained in this document. This report may not be reproduced or provided to any other person and any other person should not rely upon the contents. The distribution of this information does not constitute or form part of any offer to participate in any investment. This report does not purport to give investment advice in any way. Past performance should not be relied upon as an indication of future performance. Future performance may be materially worse than past performance and may cause substantial or total loss.